Introduction

Winning a new customer is exciting. Winning a large international order can feel like a breakthrough. But the moment between when goods ship and when payment arrives creates a cash flow gap that derails more businesses than most owners expect.

That gap is the core problem trade finance solves. Whether you're a manufacturer funding a production run, an importer managing 90-day supplier payment cycles, or an exporter waiting on overseas receivables, the mechanics of getting paid don't always align with the mechanics of getting started.

According to the WTO, 80 to 90 percent of world trade relies on trade finance — primarily trade credit and insurance. The market is enormous, the instruments are varied, and choosing the wrong one for your situation can be as costly as having no financing at all.

This guide covers what trade finance is, how it works, the key instruments available, the risks it addresses, and practical strategies for using it effectively — including alternatives when traditional banks aren't an option.

Key Takeaways:

- Trade finance bridges the gap between when exporters ship goods and when importers pay

- Core instruments include letters of credit, documentary collections, factoring, and trade credit insurance

- Instrument selection should match the risk level of the trading relationship

- Half of SME trade finance requests are rejected by traditional banks — alternative lenders fill this gap

- Documentation discrepancies are the leading cause of payment disputes — accuracy is non-negotiable

What Is Trade Finance and Why Does It Matter?

Trade finance is the set of financial instruments and techniques used to facilitate domestic and international trade. The ICC Academy defines it as services that help businesses "finance, monetise, risk mitigate, and settle trade flows" for goods and services.

The underlying tension is simple: exporters want payment before or at shipment; importers want to pay only after receiving goods. Without a third-party mechanism, one side absorbs the full risk.

The Risk Problem Trade Finance Solves

In any unstructured trade transaction, both parties face real exposure:

- The exporter ships goods with no guarantee of payment

- The importer sends funds with no guarantee of delivery

- Either scenario can result in significant financial loss

Trade finance introduces a financial intermediary — typically a bank or specialty lender — that verifies performance on both sides before releasing payment, so neither party carries the risk alone.

Key Parties in a Trade Finance Transaction

| Party | Role |

|---|---|

| Exporter/Seller | Ships goods and seeks prompt, guaranteed payment |

| Importer/Buyer | Receives goods and prefers to delay payment |

| Issuing Bank | Opens LC or guarantee on behalf of the importer |

| Advising/Confirming Bank | Notifies or guarantees payment to the exporter |

| Export Credit Agency (ECA) | Provides government-backed insurance and guarantees (e.g., EXIM Bank) |

| Trade Finance Consultant | Structures solutions and connects businesses to appropriate capital sources |

| Insurer | Covers non-payment risk from buyer default or political instability |

How Trade Finance Works: The Core Transaction Process

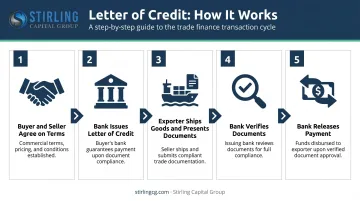

Most trade finance transactions follow a predictable sequence. Using a letter of credit as the example:

- Buyer and seller agree on terms covering price, delivery schedule, and payment method

- Importer's bank issues an LC (a formal commitment to pay once all conditions are met)

- Exporter ships goods and presents documents including the commercial invoice, bill of lading, and certificate of origin

- Bank verifies documents to confirm they match LC terms exactly

- Bank releases payment to the exporter — importer repays the bank on agreed terms

This structure shifts risk away from both parties. The exporter no longer depends on the importer's willingness to pay; the importer no longer pays before confirming shipment.

Short-Term vs. Longer-Tenor Instruments

Not all trade finance operates on the same timeline:

- Short-term (under 12 months): Most common. Used for recurring trade cycles — consumer goods, raw materials, finished products. Standard maturity is often 90 days.

- Medium-to-long-term (1–7+ years): Used for capital equipment, large infrastructure projects, and commodities. Instruments like forfaiting can extend to seven years or beyond.

The Role of Documentation

Documentation is not a formality — it's the legal and financial foundation of every trade finance transaction. Core documents include:

- Commercial invoice — states goods sold and amount due

- Bill of lading — carrier contract and proof of possession

- Packing list — itemizes shipment contents and weights

- Certificate of origin — identifies where goods were produced

- Insurance certificate — confirms cargo coverage and supports claims

Discrepancies between submitted documents and LC terms are the most common trigger for payment disputes. Even minor mismatches — a wrong date or misspelled product description — can result in payment rejection or significant delays.

Banks vs. Alternative Finance Providers

Commercial banks offer lower-cost trade finance but apply rigid credit criteria. Many SMEs don't qualify regardless of deal quality.

Alternative finance providers (AFPs) — including specialty lenders, private credit funds, and fintech platforms — move faster, accept non-standard collateral, and often serve businesses that banks decline. They typically cost more but provide access where banks cannot.

Key Trade Finance Instruments Explained

Letters of Credit

A letter of credit (LC) is a bank's written commitment to pay the exporter once specified shipping documents are presented and verified. It substitutes the bank's creditworthiness for the importer's, making it one of the most secure instruments available.

For high-risk markets or unfamiliar trading partners, a confirmed LC adds a second bank's guarantee, providing an additional layer of protection for the exporter if the issuing bank fails to pay.

Documentary Collections

Documentary collections are more cost-effective than LCs but provide less protection. The exporter's bank sends shipping documents to the importer's bank, which releases them only when the importer meets payment conditions.

Two structures apply:

- Documents Against Payment (D/P): Importer pays immediately to receive title documents. Better for the exporter.

- Documents Against Acceptance (D/A): Importer accepts a future payment obligation to receive documents. Better for the importer, but leaves the exporter with credit exposure.

Documentary collections work best for established trading relationships where trust already exists but full open-account terms aren't yet appropriate.

Export Working Capital Financing and Factoring

When payment instruments aren't enough, financing bridges the gap between fulfilling an order and getting paid. Export working capital financing provides revolving credit or transaction-specific loans to fund production, inventory, and labor before payment arrives. EXIM Bank's Working Capital Loan Guarantee backs 90% of eligible loans with no minimum transaction amount, covering inventory, finished products, and overhead costs.

Export factoring takes a different approach: the exporter sells short-term foreign receivables to a factor at a discount, receiving immediate cash. The factor assumes the collection risk. Global factoring turnover reached EUR 3,894 billion in 2024, reflecting how widely businesses use this instrument to manage cash flow.

Key benefits of factoring:

- Eliminates non-payment risk on covered receivables

- Accelerates cash conversion without waiting 30–90 days

- Does not require the same credit profile as a traditional bank loan

Trade Credit Insurance

Trade credit insurance protects exporters against non-payment due to buyer insolvency, default, or political instability. EXIM Bank's export credit insurance policies can cover up to 95% of sales invoice value.

Beyond protection, insured receivables strengthen the exporter's borrowing position. Lenders are more willing to extend working capital when foreign receivables are covered, making insurance a dual-purpose tool.

Forfaiting

Forfaiting addresses medium-to-long-term receivables, typically $100,000 or more. The exporter sells receivables at a discount on a non-recourse basis, meaning the forfaiter assumes all risk and the transaction moves off the exporter's balance sheet.

Key forfaiting features:

- Credit periods range from 180 days to seven years or more

- Frees up balance sheet capacity for additional trade

- Works alongside LCs and other payment guarantees

Key Risks Trade Finance Addresses

Every trade transaction carries layered risk. Choosing the right instrument means understanding which risks are in play.

The Four Main Risk Categories

| Risk Type | Description | Mitigation |

|---|---|---|

| Payment Risk | Buyer delays or refuses payment | LCs, documentary collections, trade credit insurance |

| Country/Political Risk | Economic instability, currency controls, regulatory changes | Political risk insurance, ECA guarantees, confirmed LCs |

| Commercial Risk | Buyer insolvency or creditworthiness deterioration | Trade credit insurance, factoring, due diligence |

| Foreign Exchange Risk | Currency fluctuation between contract and settlement | Forward contracts, FX options |

Managing FX Exposure

When exporters accept payment in a foreign currency, exchange rate movements between contract signing and payment receipt can cut into margins fast. Forward contracts allow exporters to lock in an exchange rate for delivery typically ranging from three days to one year in the future, protecting against currency depreciation.

The Compliance Layer

AML (anti-money laundering) and KYC (know-your-customer) requirements add time and cost to every trade finance transaction — particularly in emerging markets or with new counterparties. FATF flags trade-based money laundering as a persistent threat. Common red flags include:

- Document discrepancies between invoices, shipping records, and contracts

- Complex corporate structures that obscure beneficial ownership

- Transactions routed through multiple jurisdictions with no clear commercial purpose

Factor compliance timelines into your trade finance planning from the start. A deal that looks straightforward can stall once due diligence requirements kick in for a new counterparty — and that delay carries real cost if goods are already in transit.

Trade Finance Strategies and Best Practices

Strategy 1: Match the Instrument to the Relationship

Payment method selection should reflect how well you know your trading partner and how stable the trade environment is. A practical framework:

- Unknown or high-risk buyers: Cash-in-advance

- New relationships: Letters of credit

- Established relationships: Documentary collections

- Trusted long-term partners: Open account, backed by credit insurance or factoring

Overcomplicating transactions with expensive instruments when trust already exists wastes money. Underprotecting against unknown buyers creates unnecessary exposure.

Strategy 2: Use Trade Credit Insurance Before You Need It

Insurance placed reactively — after a customer shows signs of trouble — provides little protection. The best practice is to insure foreign receivables as a standard part of business operations.

Insured receivables also improve your lending position directly. As Atradius notes, lenders view insured receivables as more secure collateral, which can support larger loans, better terms, or higher credit limits.

Strategy 3: Secure Working Capital Before the Order Arrives

An approved revolving export working capital facility gives businesses the flexibility to accept large or unexpected orders without scrambling for capital under deadline pressure. Having that facility in place before an order arrives means you can move quickly when opportunities appear — not scramble to catch up after the fact.

Key steps to get there:

- Apply for an export working capital facility during a stable period, not in response to a specific order

- Work with your lender to set a credit limit that reflects your largest realistic order size

- Review and renew the facility annually so it stays current with your growth

Strategy 4: Diversify Financing Sources

Relying on a single commercial bank creates a structural vulnerability. If credit conditions tighten, that lender exits a market, or underwriting standards shift, the business has no immediate alternative.

Accessing multiple financing channels gives you fallback options and stronger negotiating position. These include commercial banks, alternative finance providers, government programs like SBA's Export Working Capital Program (up to $5 million with a 90% guarantee), and EXIM Bank.

Strategy 5: Build Document Review into Pre-Shipment

LC claims are frequently rejected on first presentation due to document discrepancies. This isn't an edge case — it's a known, recurring problem across the industry. Best practice is to:

- Align all shipping documents with LC terms before goods leave

- Involve experienced trade finance professionals in document preparation

- Build a formal document review step into the pre-shipment checklist

- Never assume documents are compliant without verification

When Traditional Bank Financing Isn't Enough

Traditional banks offer lower-cost trade finance, but they operate within rigid credit frameworks. Many SMEs, high-growth companies, or businesses in transitional situations don't qualify — regardless of the underlying deal quality.

The numbers reflect a real gap. ADB's 2025 Global Trade Finance Gap Survey estimates the global trade finance gap at $2.5 trillion. WTO data shows that roughly half of SME trade finance requests are rejected by banks, compared to just 7% for multinational corporations.

Common Reasons Businesses Seek Alternatives

Businesses typically look beyond traditional banks when:

- A bank has declined the application outright

- The deal is time-sensitive and bank approval timelines don't fit

- The collateral structure is non-standard — inventory-heavy, cross-border, or contract-based

- Growth is outpacing existing credit lines faster than the bank relationship can adapt

- The transaction is structured around confirmed purchase orders rather than balance sheet strength

How Stirling Capital Group Approaches This

Stirling Capital Group works as a commercial finance consultant (not a direct lender) with access to over 60 private lending sources — bank ABL groups, non-bank specialty finance providers, private credit funds, and trade finance-specific capital sources.

Unlike a single bank constrained to one credit box, Stirling evaluates the full transaction cycle: who the end customer is, what's being purchased or produced, when suppliers need to be paid, and how repayment flows through the revenue cycle. That transaction-based analysis, rather than a pure balance sheet review, reaches lenders that conventional bank underwriting cannot.

For manufacturers, importers, distributors, and wholesalers with strong demand but insufficient liquidity, Stirling matches the right financing structure to the actual transaction:

- Purchase order financing

- Trade finance facilities

- Revolving supply chain credit

- Receivables acceleration

Stirling offers a free consultation and business analysis. Businesses can reach the team at info@stirlingcg.com or 614-470-4716.

Frequently Asked Questions

What is trade finance?

Trade finance is a set of financial instruments — including letters of credit, trade credit insurance, factoring, and working capital facilities — designed to bridge the gap between exporters who need prompt payment and importers who prefer to pay after receiving goods. It introduces a third-party financial intermediary that manages risk for both sides of the transaction.

Is trade finance risky?

Trade finance is specifically designed to reduce risk, but residual exposures remain — including document discrepancies, buyer insolvency, and political instability. Proper instrument selection, trade credit insurance, and thorough due diligence on trading partners can significantly reduce these risks.

What are the four core functions of trade finance?

The ICC identifies four primary functions: finance (providing liquidity), monetize (converting trade assets into cash), risk mitigate (protecting against payment, political, and commercial risks), and settle (facilitating payment between parties). Different frameworks may use different terminology, but these functions underpin every trade finance product.

What is the difference between trade finance and a traditional business loan?

A traditional loan provides general-purpose capital repaid on a fixed schedule. Trade finance instruments are transaction-specific — an LC triggers on document presentation, factoring draws against existing receivables. Most trade finance is self-liquidating — the sale proceeds repay the financing directly.

What types of businesses benefit most from trade finance?

Any business buying or selling goods — manufacturers, distributors, importers, exporters, and wholesalers — can benefit. SMEs in particular gain working capital and risk protection that traditional bank loans often can't deliver for transaction-based needs.