Introduction

Many US entrepreneurs and business owners face a frustrating mismatch: they have confirmed purchase orders, solid customers, and real goods moving through real supply chains — but conventional banks still say no. The reason is structural. Traditional lenders underwrite based on your balance sheet and credit history, not the strength of the trade transaction itself.

Structured trade finance (STF) was built for this gap. It's a specialized, collateral-backed approach that draws on the value of underlying goods, receivables, and trade flows — rather than relying solely on borrower creditworthiness. Repayment is tied to the transaction's cash flows, not a fixed loan schedule.

According to the Asian Development Bank, the global trade finance gap stands at $2.5 trillion in 2025 — representing roughly 10% of global trade. SMEs bear the heaviest burden, with 41% of SME trade finance applications rejected by conventional banks.

This guide covers STF mechanics, major instrument types, who benefits most, how it stacks up against conventional lending, and the key risks to weigh before pursuing it.

Key Takeaways

- STF is underwritten against the trade transaction — goods, receivables, and cash flows — not the borrower's balance sheet

- Repayment is self-liquidating: the sale of financed goods retires the facility automatically

- Pre-export finance, warehouse financing, and receivables finance can be layered across a single trade cycle

- SMEs and mid-market companies benefit most, particularly those turned away by traditional banks

- Experienced advisors and tight documentation are critical to keeping structural and compliance risk in check

What Is Structured Trade Finance?

STF is a self-liquidating, collateral-backed form of financing built around the movement of physical goods or commodities through supply chains. The defining feature: repayment comes from the sale or export proceeds of the underlying asset, not from the borrower's general cash reserves.

Self-Liquidating — What That Actually Means

Self-liquidating means the trade transaction itself generates the repayment. When a commodity producer ships goods to a buyer and collects payment, those proceeds retire the facility. If the shipment doesn't complete, the repayment source is at risk — which is why collateral and risk structuring matter so much.

As Watson Farley & Williams describes it, STF is a "self-liquidating, collateralised, and de-risked approach to trade finance" — meaning the structure itself is designed to reduce lender exposure rather than relying on borrower strength alone.

STF vs. Standard Trade Finance

Standard trade finance covers individual instruments — a letter of credit here, a purchase order facility there. STF goes further, layering multiple tools together to finance an entire trade cycle from production through final sale. Where standard instruments cover a single transaction, STF funds the full chain of events that surrounds it.

Industries That Use It Most

STF is most common in sectors where transactions are high-value, cross-border, and commodity-driven:

- Oil and gas — large capital requirements, multi-party offtake agreements

- Metals and mining — long production cycles, volatile pricing

- Agricultural commodities — seasonal production, warehouse-held inventory

- Manufactured goods — import/export cycles with extended payment terms

What these industries share is scale and complexity — the kind that standard credit products aren't built to handle.

How Structured Trade Finance Works

STF follows a logical sequence tied to the physical movement of goods. Here's how a typical structure unfolds:

Step 1 — Transaction Assessment

Lenders evaluate the trade structure, not just the borrower's credit profile. Key factors:

- Nature of the commodity or asset being financed

- Identity and creditworthiness of all parties (producer, trader, offtaker, end-buyer)

- Cash flow projections across the trade cycle

- Supply chain risk — logistics, geography, counterparty reliability

Step 2 — Collateral Identification

Once the transaction is assessed, lenders identify what will secure it. The underlying goods, receivables, or contractual rights become collateral — packages commonly include:

- Pledges over physical goods

- Bills of lading and warehouse receipts

- Assignments of export receivables or offtake agreements

- Account-control arrangements

This gives lenders a tangible claim on value independent of the borrower's financial health.

Step 3 — Financing Across the Supply Chain

STF can be applied at multiple stages of the trade cycle, not just one entry point:

| Stage | Description |

|---|---|

| Pre-shipment | Production funding or procurement capital |

| In-transit | Financing goods while they move |

| Warehouse | Inventory-backed financing before sale |

| Post-delivery | Receivables conversion after shipment |

Multiple instruments may be layered together within one unified structure, covering the complete revenue cycle.

Step 4 — Risk Mitigation Tools

Each structure incorporates instruments matched to its specific risk profile:

- Credit insurance — protects against buyer non-payment

- Letters of credit — provide bank-backed payment assurance

- Payment guarantees — backstop counterparty obligations

- Commodity hedging — manages price volatility on collateral value

Step 5 — Repayment Aligned to Trade Cash Flows

Repayment schedules mirror actual cash inflows: buyer payments, export receipts, or inventory liquidation proceeds. This makes the structure more predictable for both sides — unlike a conventional fixed-schedule loan, timing is tied directly to the transaction itself.

Key Types of Structured Trade Finance Instruments

STF is a family of instruments, not a single product. Each is suited to a different stage of the supply chain.

Traditional Supply Chain Instruments

Pre-Export Finance (PXF) A lender advances funds to a producer or exporter before goods ship. Repayment is secured by an assignment of the export contract or offtake agreement. PXF is widely used by commodity producers who need capital to fund production.

Petroleum Development Oman's $4 billion syndicated PXF facility in 2016 shows how PXF scales to sovereign-level commodity finance.

Prepayment Financing A financier provides funds to an offtaker, who prepays the producer. Goods flow from producer → offtaker → end-buyer, and sale proceeds retire the financing. Cover ratios and top-up features manage the risk that commodity price movements reduce collateral value below the outstanding facility balance.

Warehouse Financing Goods held in storage before sale serve as collateral. IFC's Global Warehouse Finance Program demonstrates this model at institutional scale — providing liquidity backed by warehouse receipts to help agricultural producers and traders access capital without immediate forced sale. Collateral managers verify inventory quality and quantity on behalf of lenders.

Receivables-Based Instruments

Receivables Finance Two structures exist, each shifting risk differently:

- Buyer-led: The financier purchases receivables at a discount and collects full value at maturity from the buyer

- Seller-led: The financier advances a percentage against the seller's outstanding invoices and collects from the buyer directly

Forfaiting Non-recourse financing where a seller sells medium- or long-term receivables to a forfaiter at a discount. Receivables are evidenced by a bill of exchange or promissory note. The seller receives immediate liquidity; payment risk transfers entirely to the forfaiter. ICC's Uniform Rules for Forfaiting (URF 800), endorsed by the UN in 2017, govern this instrument internationally.

Who Benefits Most from Structured Trade Finance?

The primary users are commodity producers, exporters, importers, and trading companies involved in high-value, cross-border transactions. What they share: a need for financing that conventional banks either cannot or will not provide.

Why STF Works for SMEs and Mid-Market Companies

ADB data shows that 41% of SME trade finance applications were rejected in 2025. The core problem isn't transaction quality — it's that banks underwrite the borrower, not the deal. STF flips this: lenders evaluate the transaction's cash flows, collateral, and counterparty quality. A business with a strong confirmed order from a creditworthy buyer can access STF financing even if its own balance sheet is thin.

Business types that benefit most include:

- Distributors managing supplier payment timing against customer collection cycles

- Importers dealing with extended international cash conversion cycles

- Manufacturers funding raw materials and production inputs before receivables exist

- Wholesalers carrying inventory ahead of purchase order fulfillment

- Government contractors financing large confirmed contracts with delayed payment schedules

Identifying the right STF structure requires understanding both the transaction mechanics and the lender landscape. Stirling Capital Group works with businesses across these categories, matching each opportunity to specialized lenders based on the transaction's collateral, cash flow, and repayment path — not just the borrower's balance sheet.

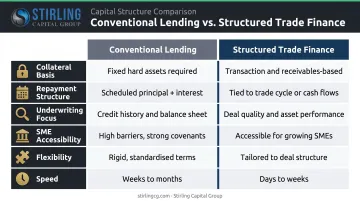

Structured Trade Finance vs. Conventional Lending

The core difference is straightforward: conventional loans are underwritten against the borrower; STF is underwritten against the transaction.

| Factor | Conventional Lending | Structured Trade Finance | |--------|---------------------|--------------------------|\n| Collateral basis | Borrower assets, real estate | Trade goods, receivables, offtake contracts | | Repayment structure | Fixed schedule | Aligned to trade cash flows | | Underwriting focus | Balance sheet, credit history | Transaction quality, counterparty strength | | SME accessibility | Restricted by credit thresholds | Transaction strength can offset borrower profile | | Flexibility | Standardized products | Structured to fit specific deal mechanics | | Speed | Slower credit committee processes | Designed for time-sensitive trade windows |

When to Choose STF Over a Conventional Loan

STF makes more sense than a conventional loan when:

- The transaction involves high-value commodities or cross-border logistics

- Jurisdictional complexity or counterparty geography exceeds bank comfort zones

- The borrower's balance sheet is thin but the trade structure is sound

- Growth is outpacing existing bank credit lines

- Speed is critical and supplier deadlines or shipping windows can't accommodate a credit committee timeline

Risks and Key Considerations

STF reduces many risks that conventional lending cannot manage — but it introduces its own.

Structural Risks

- Performance risk: The producer must deliver. If the commodity flow doesn't complete, the repayment source fails

- Credit/counterparty risk — Offtakers, end-buyers, collateral managers, and account banks must all perform as expected

- Price/market risk: Commodity price drops can reduce collateral value below the outstanding facility balance. Cover ratios and hedging instruments exist precisely to manage this

- Operational and fraud risk: Document fraud, false shipments, and forged warehouse receipts are real exposure points. ICC's 2020 Global Survey found 42% of surveyed banks reported increased fraud in 2019 across trade finance broadly

Experienced advisors and thorough due diligence address most of these risks directly. That said, structural exposure is only part of the picture — regulatory interpretation introduces a separate layer of concern.

Recharacterization Risk

Regulators can challenge whether a structured transaction constitutes unlicensed lending rather than a genuine sale or financing arrangement. Counterparties may also attempt to reclassify transactions to avoid obligations — particularly in receivables-purchase structures where retained economic recourse can make a "sale" look like a secured loan.

The mitigation: maintain meticulous transaction records, use industry-standard documentation frameworks (BAFT Master Participation Agreements, ICC URF 800), and work with advisors who understand how these structures are characterized under applicable law.

Compliance and Documentation

STF transactions require precise legal documentation:

- Facility agreements and security documents

- Offtake assignments and collateral management agreements

- Account-control arrangements and covenants

- Accurate representations to banks and underwriters

A single misrepresentation in the facility documentation can unwind the entire structure. Legal counsel familiar with trade finance structuring is not optional: improvisation here carries real structural consequences.

Frequently Asked Questions

What is structured trade finance?

Structured trade finance is a specialized, collateral-backed financing method tied to commodity flows and trade transactions. Unlike conventional lending, it focuses on the quality of the underlying transaction — the goods, receivables, and counterparties involved — rather than the borrower's balance sheet or credit history alone.

What are the 4 pillars of trade finance?

The four pillars cover every stage of a cross-border transaction:

- Payment — facilitating cross-border settlement between counterparties

- Risk mitigation — managing credit, currency, and country risk

- Financing — providing working capital across the trade cycle

- Documentation — ensuring legal clarity and compliance for all parties

How is structured trade finance different from a conventional bank loan?

STF is underwritten based on the trade transaction's cash flows and collateral — not the borrower's financial profile. Repayment mirrors the trade cycle rather than following a fixed schedule, making it accessible to businesses with strong transactions but limited balance sheet strength.

What types of businesses use structured trade finance?

Commodity producers, exporters, importers, and trading companies are the primary users — particularly SMEs and mid-market businesses in oil and gas, metals, agriculture, and manufactured goods. Many have strong transactions but don't meet conventional bank criteria.

What are the main risks in structured trade finance?

The two primary risk categories are:

- Structural risks — performance failure, counterparty default, commodity price swings, and document fraud

- Recharacterization risk — regulatory or counterparty attempts to reclassify the transaction

Proper documentation and experienced advisors are the frontline tools for managing both.

How do I get started with structured trade finance for my business?

Start with a free consultation from Stirling Capital Group. Their team evaluates your trade cycle and matches your deal to the right structure across a network of over sixty specialized lenders. Contact them at 614-470-4716, info@stirlingcg.com, or www.stirlingcg.com.