Introduction

Getting a small business loan from a traditional bank is harder than most people expect. Lenders want strong credit, years of financials, and collateral — leaving many business owners without viable options when they need capital most.

SBA loans were designed to close that gap. By partially guaranteeing loans issued through private lenders, the U.S. Small Business Administration reduces lender risk enough to open doors that conventional financing keeps shut. The SBA approved 77,600 7(a) loans totaling $37 billion in FY2025, making it one of the most active small business lending programs in the country.

This guide covers what SBA loans are, the main program types, what they cost, how to qualify, and what to do when SBA financing isn't available.

Key Takeaways:

- SBA loans are issued by private lenders and partially guaranteed by the federal government, reducing lender risk

- Four main programs cover most needs: 7(a), 504, Express, and Microloans

- Competitive rates and long repayment terms are the biggest advantages; slow timelines and strict qualification are the biggest drawbacks

- Most lenders look for a credit score around 650+, though this is a lender benchmark — not an official SBA rule

- When SBA financing isn't available, alternatives include bridge loans, equipment financing, and asset-based lending

What Is an SBA Loan and How Does It Work?

The SBA doesn't lend money directly. It guarantees a portion of loans made by approved banks, credit unions, and non-bank lenders, giving those lenders enough confidence to approve businesses they'd otherwise turn away.

The Guarantee Structure

For standard 7(a) loans, the SBA guarantees:

- Up to 85% of loans of $150,000 or less

- Up to 75% of loans above $150,000

That guarantee doesn't eliminate borrower liability — it reduces the lender's exposure if a business defaults.

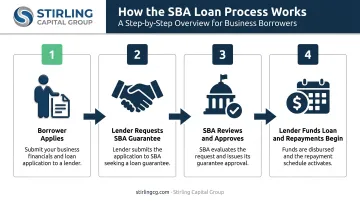

How the Process Works

The basic flow for any SBA loan:

- Borrower applies through an SBA-approved lender

- Lender requests an SBA guarantee on the loan

- SBA reviews and approves the guarantee (or the lender does, if they have delegated authority)

- Lender funds the loan and borrower begins monthly repayments

Any owner holding 20% or more of the business must sign an unlimited personal guarantee. If the business defaults, their personal assets are on the line.

Approved Uses for SBA Loan Proceeds

SBA loan funds can generally be used for:

- Working capital and operational expenses

- Real estate purchase or improvement

- Equipment, machinery, and fixtures

- Business acquisition

- Inventory and supplies

- Refinancing existing business debt

- Startup costs (program-specific)

Each program has specific permitted and prohibited uses — the 504 and microloan programs carry tighter restrictions than the 7(a).

Types of SBA Loans

The SBA runs several distinct loan programs, each built for different funding needs. Choosing the wrong program wastes time. Here's how to tell them apart.

SBA 7(a) Loans

The 7(a) is the SBA's flagship program, and the most flexible and widely used.

- Maximum loan amount: $5 million

- Repayment terms: Up to 10 years for working capital or equipment; up to 25 years for real estate

- Interest rates: Variable, negotiated with the lender, subject to SBA caps (see rate section below)

- Best for: Established businesses with multi-purpose or broad funding needs

Eligible uses include working capital, equipment, real estate, business acquisitions, and debt refinancing — making it the strongest fit when funding needs span multiple categories.

SBA 504 Loans

504 loans are purpose-built for major fixed assets: commercial real estate, land, and large equipment with a long useful life.

- Maximum amount: Up to $5 million; up to $5.5 million for certain manufacturing and energy projects

- Structure: Borrower contributes 10%, a conventional lender covers 50%, a Certified Development Company (CDC) covers 40%

- Interest rates: Fixed, tied to U.S. Treasury benchmarks

- Terms: 10-, 20-, or 25-year options

- Best for: Businesses purchasing owner-occupied commercial property or major equipment

One hard restriction: 504 funds cannot be used for working capital, inventory, or speculative real estate.

SBA Express Loans

Express loans trade loan size for speed.

- Maximum amount: $500,000

- SBA response time: Within 36 hours of lender submission

- SBA guarantee: 50% (lower than standard 7(a) loans)

- Rate cap: Slightly higher than large standard 7(a) loans for the same size loan

- Best for: Established businesses that need faster access to capital and can work within the $500,000 ceiling

That speed comes with a tradeoff: the lower guarantee percentage means lenders carry more risk, which typically results in tighter underwriting requirements.

SBA Microloans

Microloans are the entry point for smaller funding needs and less-established businesses.

- Maximum amount: $50,000 (average is around $13,000)

- Issued by: SBA-approved nonprofit intermediaries, not banks

- Maximum term: Up to 7 years

- Approved uses: Working capital, inventory, supplies, furniture, fixtures, machinery, and equipment

- Cannot be used for: Existing debt repayment or real estate purchases

- Best for: Startups, early-stage businesses, and borrowers with limited credit history

Because they're issued through nonprofit community organizations rather than conventional banks, Microloans carry more flexible underwriting, making them the most accessible SBA program for borrowers who don't yet meet standard lender thresholds.

Pros and Cons of SBA Loans

Pros

Competitive interest rates

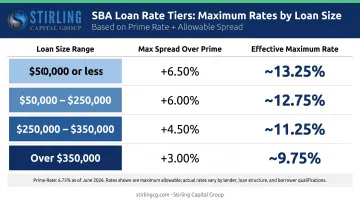

Because the SBA guarantee reduces lender risk, approved borrowers get rates well below most alternative financing. Variable 7(a) rates are capped by loan size — with the prime rate currently at 6.75% (as of June 2026), the maximum spreads are:

| Loan Size | Max Spread Over Prime | Effective Max Rate |

|---|---|---|

| $50,000 or less | + 6.5% | ~13.25% |

| $50,001 – $250,000 | + 6.0% | ~12.75% |

| $250,001 – $350,000 | + 4.5% | ~11.25% |

| More than $350,000 | + 3.0% | ~9.75% |

504 loans carry fixed rates tied to U.S. Treasury benchmarks, often lower than comparable variable-rate financing.

Long repayment terms

Up to 10 years for equipment or working capital, 25 years for real estate. Longer terms mean lower monthly payments and more cash available for operations.

High loan maximums and limited fees

7(a) and 504 loans reach up to $5 million. The SBA also restricts what lenders can charge in origination, brokerage, and application fees — keeping total borrowing costs lower than most bank or alternative lender fees.

SBA loans aren't the right fit for every situation, though. Here's where they fall short.

Cons

Strict qualification requirements

Most lenders look for:

- Personal credit score of 650 or higher (a lender benchmark, not an SBA mandate)

- At least two years of operating history (considered in underwriting, not a universal SBA requirement)

- Sufficient annual revenue to service the debt

This effectively excludes startups, businesses with recent credit problems, and those in restricted sectors like cannabis or gambling.

Slow funding timeline

Applications require extensive documentation. Approval typically takes 30 to 90 days for standard 7(a) and 504 loans. For businesses facing urgent capital needs, that timeline is a real problem.

Personal guarantees, collateral, and down payments

- All owners with 20%+ stake must sign an unlimited personal guarantee

- Loans over $50,000 typically require collateral (business assets, real estate, or equipment)

- SBA 504 loans require a minimum 10% down payment

These requirements put personal assets at risk and can be a barrier for asset-light businesses.

How to Qualify for an SBA Loan

SBA loans come with real advantages — lower rates, longer terms, and government backing — but they also come with strict eligibility requirements. Before assembling your application, confirm your business clears both the SBA's baseline criteria and your lender's underwriting standards.

Core SBA Eligibility Requirements

To be eligible for any SBA loan program, your business must:

- Operate as a for-profit entity in the U.S. or its territories

- Meet the SBA's industry-specific size standards (based on employee count or annual revenue depending on the industry)

- Be U.S. citizen or national-owned — as of March 2026, the SBA has banned foreign nationals from accessing SBA-backed loans

- Demonstrate that other financing sources have been exhausted first; the SBA only provides assistance when credit is not reasonably available elsewhere

- Have a legitimate business purpose for the funds

Financial Benchmarks Most Lenders Apply

Beyond SBA eligibility, individual lenders layer on their own underwriting criteria:

- Credit score of ~650+ is a common floor, though some SBA lenders go lower for certain programs

- Operating history matters — less than two years in business often triggers additional scrutiny

- Debt-service coverage ratio (DSCR): lenders verify that your cash flow covers loan payments with a margin of safety

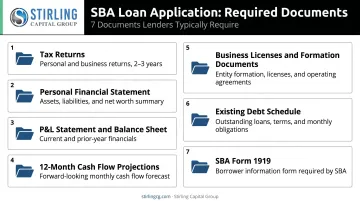

Documentation to Prepare

Gather these before starting any application:

- Personal and business tax returns (past 2–3 years)

- Personal financial statement

- Profit and loss statement and balance sheet

- 12-month cash flow projections

- Business licenses and legal formation documents (articles of incorporation, operating agreement)

- Existing debt schedule

- SBA Form 1919 (Borrower Information Form)

Common Disqualifying Factors

- Recent bankruptcies, tax liens, or unresolved judgments

- Operating in an ineligible industry (gambling, certain financial businesses, speculative ventures, non-profits, and others listed under 13 CFR 120.110)

- Insufficient collateral or equity contribution

- Failure to demonstrate that other financing sources were pursued first

Cross-check the SBA's ineligible business list early — it's faster to rule out disqualifying factors before building your full documentation package.

How to Apply for an SBA Loan Step by Step

Step 1 — Confirm Eligibility and Choose the Right Program

Match your funding need to the right program before doing anything else:

- 7(a): Flexible, multi-purpose funding up to $5 million

- 504: Major fixed assets (real estate, large equipment) with a 10% down payment

- Express: Faster access to capital up to $500,000

- Microloan: Smaller amounts, more flexible qualification, up to $50,000

Starting in the wrong program means restarting the process from scratch — so confirm your fit before you approach any lender.

Step 2 — Find an SBA-Approved Lender

Use the SBA's Lender Match tool to connect with participating lenders — more than 800 lenders use the platform across all 50 states.

Prioritize SBA Preferred Lenders (PLP status). These lenders have delegated authority to approve loans without sending them to the SBA for review, which significantly reduces the timeline. Ask any potential lender about their annual SBA loan volume and experience with the specific program you need.

Step 3 — Gather and Organize Your Documentation

Compile everything before submitting — incomplete documentation is the most common reason applications stall or get denied. At minimum, expect to provide business tax returns (2–3 years), personal financial statements, a current P&L and balance sheet, a business plan or use-of-funds summary, and any applicable collateral documentation. Stay responsive when lenders ask follow-up questions; gaps in documentation can add weeks to your timeline.

Step 4 — Submit and Follow Through

Once submitted, timelines vary:

- A few weeks with a Preferred Lender (especially for Express loans)

- 30–90+ days for standard 7(a) or 504 applications

Respond quickly to any lender requests — slow responses on your end are one of the most common and easily avoided causes of delay. After approval, the lender manages closing and fund disbursement. If the process feels complex or your situation doesn't fit a standard bank's criteria, working with a capital advisor can help you identify the right lender and keep the application moving.

When an SBA Loan Isn't the Right Fit

SBA programs don't work for everyone. Common scenarios where businesses fall outside the SBA's reach:

- Less than two years in operation

- Credit scores below the 650 lender benchmark

- Operating in an ineligible industry

- Urgent funding needs that can't wait 1–3 months

- Loan purpose doesn't align with any SBA program

If you've been denied, that's not the end. Request written feedback from the lender to understand the specific reason. Work on improving credit or financial documentation, and consider reapplying in 6–12 months if the underlying issue is fixable.

Whether the denial is temporary or the SBA simply isn't the right structure, other financing paths are worth considering:

- Conventional commercial loans for established businesses with strong financials and bank relationships

- Equipment financing secured directly against the machinery or capital assets being purchased

- Bridge loans for time-sensitive acquisitions or transitional situations that can't wait on bank timelines

- Asset-based lending (ABL) using revolving credit structures backed by receivables, inventory, or equipment

- Private debt or equity capital for growth, acquisition, or recapitalization scenarios outside conventional credit boxes

Stirling Capital Group works across all of these categories, with access to more than 60 private lending sources including non-bank lenders, private credit funds, and specialty finance providers. For businesses that have been bank-declined or don't fit the SBA mold, a free consultation can help identify which financing path — SBA or otherwise — fits the situation. Reach out at info@stirlingcg.com or 614-470-4716.

Frequently Asked Questions

What is an SBA loan?

An SBA loan is a small business loan issued by a bank or approved lender and partially guaranteed by the U.S. Small Business Administration. The government guarantee reduces lender risk, allowing small businesses to access lower rates and longer repayment terms than most would qualify for on their own.

Who is eligible for an SBA loan?

Eligibility requires a for-profit U.S.-based business that meets SBA size standards, U.S. citizen or national ownership, demonstrated repayment capacity, and evidence that other financing sources were pursued first. SBA Microloans have more flexible requirements, making them accessible to startups and borrowers with limited credit history.

What is the easiest SBA loan to get approved for?

SBA Microloans are generally the most accessible, with flexible underwriting through nonprofit intermediaries and no requirement for collateral or real estate. SBA Express loans offer faster approvals for established businesses that need capital within the $500,000 limit.

How long does it take to get an SBA loan?

Timelines range from a few weeks with an SBA Preferred Lender (particularly for Express loans) to 30–90 days for standard 7(a) or 504 applications. Submitting complete documentation upfront and working with an experienced lender are the most effective ways to avoid delays.

What is the $10,000 SBA grant?

This refers to the COVID-19 Emergency EIDL Advance, which provided up to $10,000 to pandemic-affected businesses — a program now closed as of January 1, 2022. All current SBA programs are loan-based and require repayment.

Can you get an SBA loan with bad credit?

Most SBA lenders look for a personal credit score around 650 or higher. SBA Microloans offer the clearest path for borrowers with limited or imperfect credit, since nonprofit intermediaries use more flexible underwriting standards than conventional banks.