Introduction

You've delivered the work. You've sent the invoice. Now payroll is due Friday, a supplier needs payment, and your next project requires materials you can't afford to buy yet. The revenue exists — it's just sitting in someone else's accounts payable queue on net-60 terms.

According to QuickBooks' 2025 Small Business Late Payments Report, 56% of U.S. small businesses are currently owed money from unpaid invoices, with the average sitting at $17,500. For most of them, it's not a cash flow problem — it's a timing problem.

Invoice funding solves exactly this. It converts outstanding invoices into immediate working capital without taking on traditional debt or waiting for clients to pay on their own schedule. What follows breaks down how it works, what it costs, who qualifies, and how to match the right structure to your situation.

Key Takeaways

- Businesses typically receive 80%–90% of invoice value upfront, often within 24–48 hours

- Two main structures: invoice factoring (selling the invoice) and invoice financing (borrowing against it)

- Costs run 1%–5% of invoice value per billing cycle — not a fixed interest rate

- Approval depends on your customers' creditworthiness, not your credit score

- Works best as a short-term cash flow bridge — most effective when used selectively, not as an ongoing financing crutch

What Is Invoice Funding?

Invoice funding is an umbrella term for financing solutions that unlock cash from unpaid invoices: either by selling those invoices outright or using them as collateral for a short-term advance.

Invoice Factoring vs. Invoice Financing

These two structures work differently and suit different situations:

Invoice Factoring

The business sells its invoices to a factoring company at a discount. The factor collects payment directly from the client and remits the remaining balance (minus fees) back to the business. Collection responsibility transfers entirely.

Invoice Financing (Accounts Receivable Financing)

The business uses unpaid invoices as collateral to secure an advance from a lender. The business retains invoice ownership, keeps collecting from the client, and repays the advance plus fees once payment arrives.

Invoice financing keeps the client relationship intact and confidential: your customer never knows you've borrowed against their invoice. With factoring, the factor may contact your customer directly, which some clients notice.

What Invoice Funding Is Not

Invoice funding doesn't add long-term debt to your balance sheet the way a traditional loan does. It doesn't require hard collateral like real estate, and approval doesn't hinge on your personal credit score.

Under accounting standards, a factoring transfer structured as a true sale removes the receivable from your balance sheet entirely. If the criteria for a true sale aren't met, the lender treats it as a secured borrowing instead.

Who Uses It

Invoice funding is designed for B2B companies that invoice other businesses or government agencies under extended payment terms: net-30, net-60, or net-90. Industries with the highest usage include:

- Manufacturing and wholesale distribution

- Staffing and professional services

- Logistics and freight

- Construction and government contracting

Atradius's 2025 Payment Practices Barometer found that 57% of U.S. B2B suppliers already use invoice financing in some form.

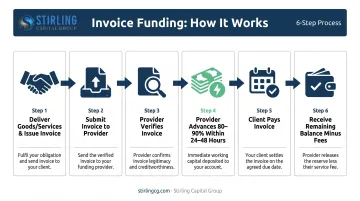

How Invoice Funding Works: Step-by-Step

The process follows a consistent sequence regardless of the provider:

- Deliver goods or services and issue an invoice to your client

- Submit the invoice to your funding provider with relevant details

- Provider verifies the invoice — checking that it's valid, undisputed, and that your client has a reliable payment history

- Provider advances 80%–90% of the invoice value, typically within 24–48 hours

- Client pays the invoice on their normal terms

- You repay the advance plus fees and receive the remaining balance

Here's what those steps look like in practice with real numbers.

Concrete Example: $25,000 Invoice on Net-60 Terms

Assume an 85% advance rate and a 3% monthly factoring fee:

| Scenario | Invoice Value | Advance (85%) | Fee | Net Received |

|---|---|---|---|---|

| Client pays in 30 days | $25,000 | $21,250 | $750 (3%) | $20,500 |

| Client pays in 60 days | $25,000 | $21,250 | $1,500 (6%) | $19,750 |

The fee doubles if your client takes the full 60 days — so slow-paying customers directly increase your cost of capital. Confirming client payment habits before submitting an invoice is worth the effort.

The Verification Step

During verification, providers review the invoice's age and legitimacy, check the client's creditworthiness (not your personal credit), and may request an accounts receivable aging report or recent bank statements. Approval hinges on your customer's ability to pay. Your own credit history is largely irrelevant to the decision.

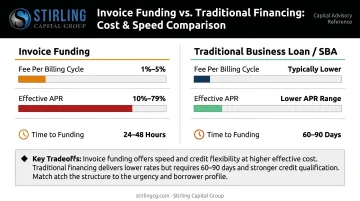

Speed Advantage

Most invoice funding providers approve and fund within 24–48 hours of verifying a valid invoice. Compare that to an SBA loan, where the end-to-end process from application to funding typically runs 60–90 days. For businesses managing tight operating cycles, that 60-day gap can mean the difference between meeting payroll and missing it.

Types of Invoice Funding

Invoice Factoring vs. Invoice Financing

| Invoice Factoring | Invoice Financing | |

|---|---|---|

| Who collects from client? | The factoring company | Your business |

| Client visibility? | Yes — factor contacts client | No — confidential |

| Best for | Businesses wanting to offload collections | Businesses preserving client relationships |

| Typical cost | Higher (factor absorbs more risk) | Varies by lender |

Recourse vs. Nonrecourse Factoring

Within factoring, there's an important distinction:

- Recourse factoring: If your client doesn't pay, you're responsible for buying the invoice back. Lower fees, but you carry the default risk. This is the most common arrangement.

- Nonrecourse factoring: The factoring company absorbs the loss if your client defaults. Higher fees reflect the added risk they're taking on.

Additional Structures to Know

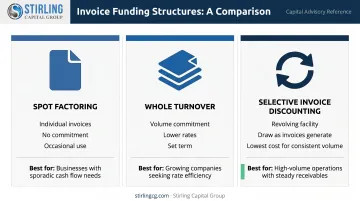

- Spot factoring: Sell individual invoices as needed — no long-term commitment or monthly minimums. Useful for occasional cash flow gaps.

- Contract factoring: Factor most invoices over a set term, typically at lower rates in exchange for volume commitment

- Receivables-based line of credit: A revolving credit facility tied to outstanding receivables. Draw as invoices are generated, repay as clients pay — often the lowest-cost option for businesses with consistent invoice volume.

Choosing between these structures isn't always straightforward — the right fit depends on your client relationships, invoice volume, and cost tolerance. A commercial finance advisor like Stirling Capital Group can pull together lender comparisons across factoring, invoice financing, and ABL revolving facilities from a network of over 60 private lending sources, saving weeks of independent research.

What Does Invoice Funding Cost?

The Primary Fee

Invoice funding isn't free — and understanding the fee structure upfront prevents surprises. The core charge is the factoring or financing fee, expressed as a percentage of invoice value, typically 1%–5% per billing cycle, accruing based on how long the invoice remains unpaid.

Some providers charge a flat fee upfront. Others accrue weekly or monthly. The structure matters — weekly accrual can get expensive fast.

How Fees Add Up Over Time

Using a 3% monthly fee on a $10,000 advance:

| Days Until Client Pays | Effective Fee | Total Cost |

|---|---|---|

| 30 days | 3% | $300 |

| 45 days | 4.5% | $450 |

| 60 days | 6% | $600 |

A client who pays two weeks late doubles your cost. Build that into your pricing analysis before committing to any arrangement.

Additional Fees to Watch

Not all costs appear in the headline rate. Common additional charges include:

- Origination or setup fees

- Monthly service or administration fees

- Credit check fees

- ACH or wire transfer fees

- Monthly minimum volume fees

- Early termination fees

Request a full fee disclosure before signing anything. Ask specifically what happens if a client pays late, and whether any fees are charged regardless of invoice volume.

The APR Reality

When short-term fees are annualized, invoice funding costs more than it appears. According to NerdWallet, invoice factoring can carry effective APRs ranging from 10% to 79% depending on repayment speed — with a 3% fee on a 30-day invoice translating to roughly 42% APR. That's well above what most business loans or credit lines carry. The tradeoff is speed and access — particularly for businesses that can't qualify for traditional financing.

Pros and Cons of Invoice Funding for Small Businesses

Advantages

- Fast liquidity: Funding within 24–48 hours vs. 60–90 days for SBA loans

- Credit-flexible approval: Based on your clients' creditworthiness, not your credit score — making it accessible for businesses declined by traditional banks

- No long-term debt: Repaid when your client pays, not on a fixed monthly schedule

- Scales with revenue: More invoices means more available capital — the facility grows with your business

- Confidential option: Invoice financing lets you access capital without notifying your clients

Disadvantages

- Higher effective cost: APRs can reach 40%+ when fees are annualized

- Late-paying clients compound costs: Every extra week a client takes increases your fee

- Recourse risk: Most arrangements leave you liable for unpaid invoices if a client doesn't pay

- B2B only: Not available for B2C businesses or those without consistent invoice volume

- Dependency risk: Addresses cash flow timing but not underlying profitability problems — repeated use can mask a deeper financial issue

Who Qualifies for Invoice Funding?

Standard Qualification Criteria

Providers typically evaluate:

- Valid, undisputed B2B or B2G invoices for work already completed or goods already delivered

- Creditworthy clients with a track record of paying on time

- No existing liens on accounts receivable — a prior lender's lien on your receivables can disqualify you

- Some operating history — requirements vary by lender, but many prefer 6+ months in business; some specialty lenders will work with newer businesses on a case-by-case basis

Industries Most Commonly Served

Invoice funding is accessible across a wide range of B2B industries:

- Manufacturing and industrial products

- Staffing and temp agencies

- Transportation and logistics

- Construction and contractors

- Healthcare services

- Professional and business services

- Wholesale distribution, importers, and exporters

- Government contractors

Note for construction and healthcare businesses: These industries involve complex billing structures — retainage, AIA pay applications, and lien waivers in construction; insurance-based receivables and Medicare/Medicaid payment cycles in healthcare. Both require lenders with specialized underwriting experience in those billing environments.

The Credit Flexibility Angle

Because approval is driven by client creditworthiness, invoice funding is one of the more accessible financing options for businesses that have been declined by traditional banks. The Federal Reserve's 2026 Small Business Credit Survey found that 22% of small employer firms received no funding at all when applying for financing — invoice funding offers an alternative path for many of them.

For businesses in this position, a commercial finance advisor can identify lenders that don't appear in a standard direct-lender search — particularly for non-standard receivables like government contracts or healthcare billing.

Stirling Capital Group works with over 60 private lending sources, including non-bank ABL lenders, private credit funds, and specialty finance providers experienced in those categories. Each deal is pre-qualified and pre-underwritten before lenders are approached, so borrowers enter those conversations from a stronger position.

Frequently Asked Questions

What is invoice funding?

Invoice funding is a financing method that allows businesses to access cash tied up in unpaid invoices — either by selling those invoices to a third party (factoring) or borrowing against them as collateral (invoice financing) — without waiting for clients to pay on standard terms.

How quickly can I get funds with invoice funding?

Most providers can approve and fund within 24–48 hours of verifying a valid invoice, making it far faster than traditional bank loans or SBA financing, which typically takes 60–90 days from application to funding.

What is the average cost of invoice funding?

Fees typically range from 1% to 5% of invoice value per billing cycle, with effective APRs commonly ranging from 10% to 79% depending on fee structure, invoice size, and how quickly your client pays.

Is invoice funding a good option for businesses with bad credit?

Approval is based primarily on your clients' creditworthiness rather than your own credit score, making it one of the more accessible financing options for businesses with limited or imperfect credit history.

What types of businesses qualify for invoice funding?

Invoice funding is designed for B2B businesses that regularly invoice other companies or government agencies under net-30 to net-90 payment terms. It's most common in staffing, manufacturing, logistics, construction, healthcare, and professional services.

What is the difference between invoice funding and a traditional business loan?

Unlike a traditional loan, invoice funding doesn't create long-term debt and doesn't require hard collateral or a strong credit score. Repayment happens when your client pays the invoice, not on a fixed monthly schedule.