Introduction

Most construction projects don't fail during the build — they fail at the financing stage. Wrong loan structure, unexpected rate resets, or a second approval falling through mid-project can unwind months of planning before a single wall goes up.

Construction-to-permanent financing is a single loan product that covers both the construction phase of a new build and converts automatically into a long-term mortgage upon completion. Most lenders call it a "one-time close" or "single-close" loan.

For developers, investors, and builders, this structure eliminates the need to apply for two separate loans — reducing closing costs, approval uncertainty, and rate exposure. It also locks in permanent financing terms before breaking ground, which matters when rates move fast. That said, it comes with specific qualification requirements and process nuances that catch even experienced borrowers off guard.

This guide covers how it works, what lenders actually look for, where the real risks sit, and when a different financing structure might serve you better.

Key Takeaways

- Construction-to-permanent financing combines a construction loan and permanent mortgage into one product, with a single closing and one set of closing costs.

- Funds are disbursed in milestone-based stages ("draws"); borrowers pay interest only on amounts drawn.

- Approval requires blueprints, a line-item budget, a licensed contractor, and an as-completed appraisal.

- Standard eligibility benchmarks: 680+ credit score, 20% down payment, DTI below 45%.

- Private and specialty lenders offer more flexible underwriting than traditional banks for complex or non-standard projects.

What Is Construction-to-Permanent Financing?

Construction-to-permanent financing serves one specific purpose: funding a new property build from the ground up, then converting into a standard mortgage once a certificate of occupancy is issued. Construction-to-permanent financing serves one specific purpose: funding a new property build from the ground up, then converting into a standard mortgage once a certificate of occupancy is issued. The entire process runs under a single approval and one closing.

This structure eliminates one of the biggest risks in construction lending: completing a build, then having to re-qualify and re-close on a separate mortgage months later under potentially different market conditions. Fannie Mae confirms that single-closing transactions allow lenders to underwrite and close both the construction loan and the permanent financing simultaneously using one set of documents.

Construction-to-Permanent vs. Construction-Only Loans

A construction-only (or "stand-alone") loan covers the build phase only. When construction ends, the borrower must separately apply and qualify for a permanent mortgage to pay it off — two closings, two sets of fees, and renewed exposure to rate changes.

| Feature | Construction-to-Permanent | Construction-Only |

|---|---|---|

| Closings | 1 | 2 |

| Closing cost sets | 1 | 2 |

| Rate lock | At initial closing | After construction |

| Re-qualification required | No | Yes |

| Flexibility to shop rates | Limited | Yes |

The two-loan approach makes sense in specific situations: if you plan to sell the completed property rather than hold it, or if your preferred construction lender doesn't offer a conversion option.

How Construction-to-Permanent Financing Works

The end-to-end flow: you qualify once for the full loan amount covering land, construction costs, and the permanent mortgage. The lender disburses funds to the builder in stages during construction. Upon completion, the loan converts automatically to a standard mortgage and regular principal-plus-interest payments begin.

Phase 1: Application and Approval

At this stage, lenders evaluate two things simultaneously: the borrower and the project.

Borrower evaluation includes:

- Credit score, income, DTI ratio, and liquid assets

- Verification of sufficient reserves to cover potential cost overruns

Project evaluation includes:

- A formal as-completed appraisal (valuing the property as if fully built)

- Detailed architectural plans, blueprints, and a line-item construction budget

- Builder's license and credentials verification

- Proof of permits or permit-readiness

This single approval covers both the construction and permanent loan phases, which is why the upfront documentation burden is heavier than a standard mortgage application.

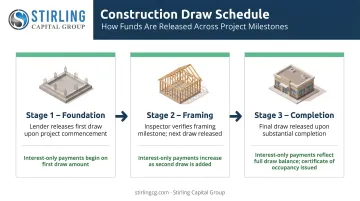

Phase 2: The Construction Draw Schedule

Rather than releasing the full loan amount at closing, the lender disburses funds in stages tied to completed construction milestones. U.S. Bank describes typical draw points including foundation, framing, and subsequent construction phases, with each draw requiring lender inspection to verify completed work before funds are released.

During the construction phase:

- Borrowers make interest-only payments on the disbursed balance — not the full loan amount

- Monthly payments start low and increase as more funds are drawn

- The lender sends an inspector before each draw release to confirm milestone completion

This keeps carrying costs manageable as construction progresses — and sets up a clean transition into the permanent mortgage phase.

Phase 3: Conversion to Permanent Mortgage

Once the build is complete and a certificate of occupancy is issued, the loan converts to the permanent mortgage under the interest rate and terms locked in at the original closing. Regular monthly principal-and-interest payments begin on the full loan balance.

Watch the timeline: Some lenders require updated financial documentation at conversion if the construction phase runs long. Fannie Mae's single-closing guidelines set firm limits:

- 12 months maximum for any single construction period

- 18 months total from original closing to conversion

Projects that exceed these thresholds can create complications at the conversion stage, so build scheduling into your financing plan from day one.

Eligibility Requirements for a Construction-to-Permanent Loan

Because construction lending involves funding a property that doesn't yet exist, lenders treat it as higher risk than a standard mortgage. Qualification criteria reflect that.

Borrower Requirements

Conventional lender benchmarks:

- Credit score of 680 or higher

- DTI ratio at or below 45%

- Sufficient liquid assets to cover the down payment, reserves, and potential cost overruns

- Stable, documentable income

Government-backed alternatives:

- FHA: down payment as low as 3.5% for eligible borrowers (minimum credit score applies)

- VA: no down payment required for eligible veterans with full entitlement; no VA-mandated minimum credit score, though lenders typically expect around 620

Project Requirements

Lenders must approve both the borrower and the project. Required project documentation typically includes:

- A formal as-completed appraisal from a licensed appraiser

- Detailed architectural plans and blueprints

- A signed contract with a vetted, licensed general contractor

- A line-item construction budget

- Proof of permits or permit-readiness

Down Payment Calculation

Conventional construction-to-permanent loans typically require 10–20% down, calculated on the full projected value of the completed property.

Example: If your land costs $200,000 and construction costs are $600,000, your total project value is $800,000. At 20% down, your down payment is $160,000. Fannie Mae's guidelines confirm that LTV is calculated by dividing the loan amount by the as-completed appraised value of the property, including the lot and improvements.

These requirements assume a conventional bank approval path. Developers with non-W2 income, recent credit events, or complex project structures often fall outside standard underwriting parameters — and get declined despite viable projects. Capital advisory firms like Stirling Capital Group work with over 60 private and specialty lenders, including groups that specifically focus on projects conventional institutions won't touch. That breadth of lender access can make a significant difference when your deal doesn't fit a standard credit box.

Pros, Cons, and Common Misconceptions

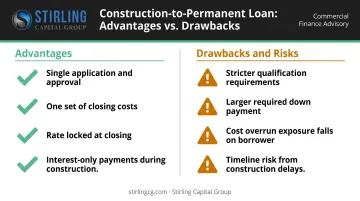

Advantages of Construction-to-Permanent Financing

- Single application and approval — no re-qualifying mid-project

- One set of closing costs — saves thousands compared to the two-loan approach

- Rate locked at closing — protects against rate increases during the build; Wells Fargo notes extended rate locks can secure a rate for 6 to 12 months

- Interest-only payments during construction — reduces financial burden while the property isn't yet producing income

Drawbacks and Risks

- Stricter qualification than standard mortgages — both borrower and project must be approved

- Larger required down payment in most conventional programs

- Cost overrun exposure — if the build exceeds the approved budget, the borrower covers the difference out of pocket

- Timeline risk — construction delays from weather, permitting, or contractor issues can push the project past the lender's allowed construction period, creating conversion complications

Common Misconceptions

These risks connect directly to a few persistent myths worth addressing before you commit to a structure.

"The loan adjusts if costs run over." It doesn't. The loan amount is fixed at closing. Overruns are entirely the borrower's responsibility. NAHB's 2024 construction cost survey found construction costs represented 64.4% of the average new-home price, with finished lot costs adding another 13.7%. Budget tightly.

"Interest-only payments mean no financial strain." Borrowers often may still be paying rent or carrying other housing costs simultaneously during the construction period. The reduced payment helps, but doesn't eliminate the carrying burden.

"Construction-to-permanent loans are only for residential builds." This structure also applies to commercial properties — multifamily developments, mixed-use projects, hospitality, industrial, and more. Commercial versions carry different underwriting criteria and are typically accessed through private, specialty, or institutional lenders rather than traditional banks.

When Construction-to-Permanent Financing May Not Be the Right Fit

This structure isn't the right answer for every project. Consider alternatives in these situations:

When a construction-only loan makes more sense:

- You plan to sell the completed property rather than hold it — a permanent mortgage conversion isn't needed

- Your construction timeline exceeds the lender's maximum allowed construction period (typically 18 months for conventional programs)

When a renovation loan may be more appropriate:

- The project involves significant renovation to an existing structure rather than true ground-up construction — FHA 203(k) or commercial renovation loan programs are better suited here

When a two-close structure may offer more flexibility:

- You're building in a complex permitting environment

- The project is mixed-use or involves non-traditional contractors that conventional C-to-P programs won't accept

- You want the option to shop for permanent financing rates after the build is complete

The right financing structure depends on your exit strategy, project timeline, financial profile, and lender relationships. For borrowers whose projects don't fit a standard program, Stirling Capital Group can evaluate multiple construction lending options — including ground-up construction loans, mezzanine financing, and permanent stabilization financing — across its network of private and specialty lenders.

Stirling Capital Group's construction financing spans projects from $5 million to $500 million and beyond, across asset classes ranging from multifamily and hospitality to mixed-use and industrial.

Frequently Asked Questions

How does a construction-to-permanent loan work?

The loan funds construction through a draw schedule tied to completed milestones, with borrowers paying interest only on disbursed amounts. Once construction is complete and a certificate of occupancy is issued, the loan converts automatically to a permanent mortgage — one application, one closing, no re-qualification required at conversion.

Do construction-to-permanent loans require a down payment?

Yes. Conventional programs typically require 10–20% down, calculated on the total projected value of land plus construction. Government-backed programs (FHA, VA) allow lower down payments for eligible borrowers.

Is it hard to get approved for a construction-to-permanent loan?

More demanding than a standard mortgage: lenders underwrite both the borrower and the project simultaneously. Typical requirements include a 680+ credit score, detailed construction plans, a licensed contractor, and formal project approval. Traditional banks are especially strict; private lenders offer more flexibility for complex borrower profiles.

What is the monthly payment on a $300,000 construction loan?

During construction, you pay interest only on the amount drawn — not the full $300,000 — so payments start low and increase as draws are released. At a fully drawn balance and current benchmark rates near 6.47%, interest-only payments run approximately $1,618/month. At conversion to a 30-year permanent mortgage, principal-and-interest payments on $300,000 at 6.47% are approximately $1,891/month, excluding taxes, insurance, and fees.

What is the difference between a construction-to-permanent loan and a construction-only loan?

A construction-to-permanent loan converts into a long-term mortgage at completion: one closing, one set of costs. A construction-only loan covers just the build phase; the borrower must apply for and close a separate mortgage afterward, resulting in two closings and two sets of fees.

Can construction-to-permanent financing be used for commercial properties?

Yes. Construction-to-permanent structures are available for commercial projects including multifamily, mixed-use, industrial, and hospitality. Underwriting requirements differ significantly from residential products, and these loans are typically sourced through private, specialty, or institutional lenders rather than traditional banks.