Introduction

You land a $500,000 order from a major retailer. It's exactly the growth opportunity you've been chasing. Then reality sets in: you don't have the cash to pay your supplier upfront, and the order ships in six weeks. Turning down the deal feels wrong. Taking it without funding could sink you.

This is where purchase order (PO) financing comes in. According to the Federal Reserve's 2024 Small Business Credit Survey, over half of small business owners cited uneven cash flows as a primary financial challenge — and large orders are one of the most common triggers.

PO financing is a short-term, transaction-specific funding tool that pays your supplier directly so you can fulfill confirmed customer orders without burning through working capital. This guide covers how it works, who qualifies, what it costs, and when it makes sense.

Key Takeaways

- PO financing pays your supplier directly (up to 100% of costs) so you can fulfill large orders without equity dilution or new long-term debt

- Approval centers on your customer's creditworthiness, not yours — making it accessible to startups and businesses with thin credit histories

- Fees typically run 1%–6% per month, translating to 20%–50%+ APR, which is significantly higher than traditional loans

- PO financing works pre-shipment while invoice factoring works post-shipment; the two can be combined sequentially

- Minimum order sizes and gross margin thresholds apply; most lenders require at least $50,000 and 20–25% gross margins

What Is Purchase Order (PO) Financing?

PO financing is a short-term cash advance where a financing company pays your supplier directly (covering up to 100% of supplier costs) so you can fulfill a confirmed customer order without depleting working capital.

This is not a traditional loan. There's no general credit line, no monthly repayment schedule, and no traditional collateral requirement. The deal is tied to one specific transaction and repaid once your customer pays their invoice.

The Purchase Order as Collateral

In this context, a purchase order is more than a business document. Under UCC Article 2, a purchase order functions as a legally binding contract upon acceptance or fulfillment by both parties. It confirms the intent to purchase specific goods at an agreed price — and it serves as the foundational collateral that makes PO financing possible.

Without a confirmed, non-cancelable PO from a creditworthy buyer, there's no deal to finance.

The Four Parties Involved

That collateral structure also determines who's involved. Every PO financing transaction runs through four distinct parties:

| Party | Role |

|---|---|

| Your business | Receives the customer order; applies for financing; fulfills and delivers goods |

| PO financing company | Evaluates the deal; pays the supplier directly; collects from the customer |

| Supplier | Receives direct payment; produces and ships goods |

| End customer | Issues the original purchase order; pays the financing company upon delivery |

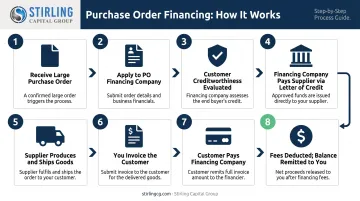

How Does Purchase Order Financing Work?

The process follows a clear sequence from order to repayment:

- You receive a large purchase order you can't fund with existing cash

- You apply to a PO financing company, submitting the purchase order and supplier cost estimate

- The financing company evaluates your customer's creditworthiness — not yours — and approves funding

- The financing company pays your supplier directly, often via a letter of credit

- Your supplier produces and ships the goods to your end customer

- You invoice the customer

- The customer pays the financing company directly

- The financing company deducts its fees and remits the remaining balance to you

The Role of the Letter of Credit

Rather than wiring cash immediately, many PO financing companies issue a letter of credit (LC) to the supplier. An LC is a bank-backed payment guarantee confirming that payment will be released once the supplier provides proof of shipment. This reduces risk for the supplier, the financing company, and your business — and is standard practice in international trade transactions.

PO Financing May Not Cover 100% of Supplier Costs

The financing company won't always cover 100% of supplier costs. If they approve only 80–90%, your business must cover the difference out of pocket. Calculate your gap amount before applying so you have a funding plan ready for that shortfall.

A Concrete Example

Scenario: A mid-sized apparel distributor — let's call them Apex Brands — receives a $500,000 purchase order from a national retailer.

- Apex's overseas supplier costs: $350,000

- PO financing company funds: $350,000 directly to the supplier via LC

- Supplier ships goods; retailer accepts delivery

- Retailer pays the financing company: $500,000

- Financing company deducts fees (say, 2%/month over 60 days = $14,000)

- Apex receives: $136,000 net profit

Unlike a business loan, there are no monthly payments. The advance is repaid in full when the customer pays — which means repayment is tied directly to the transaction, not your monthly cash flow.

Who Qualifies for Purchase Order Financing?

Core Eligibility Requirements

Most PO financing companies require all of the following:

- Tangible, finished goods — services, raw materials, and partially manufactured products don't qualify

- B2B or B2G customers (direct-to-consumer sales are excluded)

- Creditworthy end customers — lenders underwrite primarily against your buyer, not you

- Gross profit margins of 20–25% or higher — lenders need enough margin to absorb fees and risk

- Verifiable suppliers that lenders can confirm and pay directly

Your own credit score matters far less than your customer's ability to pay — which is why PO financing is accessible even to startups and businesses with imperfect credit histories.

Who Benefits Most

PO financing is most commonly used by:

- Manufacturers and contract producers

- Distributors, wholesalers, and importers/exporters

- Government contractors (B2G)

- Seasonal product businesses with inventory spikes

- Startups that have landed large initial orders but lack capital

If your business falls into any of these categories, you're likely a strong candidate — provided your end customer has solid credit.

Documentation You'll Need

Gather these before applying:

- Customer's purchase order (confirmed, non-cancelable)

- Supplier invoice or quote

- Business financial statements

- Business and personal tax returns

- Basic business information and entity documents

Minimum Order Thresholds

Having your documents ready speeds up approval considerably. That said, lenders also apply size minimums before any review begins.

Most lenders require a minimum purchase order of $50,000, though some specialty lenders start at $100,000. Orders involving unproven customers or unvetted suppliers face heightened scrutiny and may be declined.

Pros and Costs of PO Financing

The Upside

PO financing solves a specific and painful problem: turning down a large order because you can't fund the supplier payment. The core benefits:

- Accept orders you'd otherwise lose — no equity dilution, no long-term debt

- Faster than bank financing — approval typically takes 24–48 hours after documentation is submitted, with funding within days

- Accessible to non-traditional borrowers — lenders evaluate the customer, not just you

- Preserves ownership — you're not giving up equity to fund growth

This makes it especially valuable for fast-growing companies, seasonal businesses, and government contractors with extended payment cycles.

The Cost Reality

PO financing is not cheap. According to NerdWallet, fees typically range from 1% to 6% per month on supplier costs.

Monthly fees look modest in isolation, but the annualized cost tells a different story.

Illustrative calculation:

- Supplier advance: $100,000

- Fee rate: 2% per month

- Financing period: 60 days (2 months)

- Total fees: $4,000

- Annualized equivalent: roughly 24% APR

Forbes Advisor estimates PO financing APRs range from 20% to 50% — significantly higher than a traditional business line of credit, which the Kansas City Fed reports carries median rates around 7%–7.5%. The cost is the trade-off for speed and access when traditional credit isn't available.

The Drawbacks

Beyond cost, PO financing carries operational and structural risks worth understanding before you commit:

- Loss of control — the financing company pays your supplier and collects from your customer directly, putting your key relationships in a third party's hands. Vet lender communication practices before signing.

- Partial approval — if the lender only covers 80% of supplier costs, you're on the hook for the rest

- Customer non-payment — if your customer doesn't pay, you may still owe the financing company. Never use PO financing on orders from customers whose creditworthiness you can't verify.

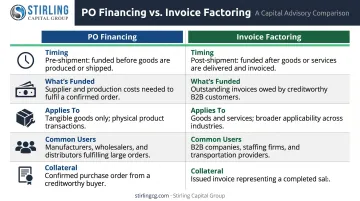

PO Financing vs. Invoice Factoring: Key Differences

These two products are frequently confused — but they operate at different points in the transaction cycle.

| PO Financing | Invoice Factoring | |

|---|---|---|

| Timing | Pre-shipment (before goods are delivered) | Post-shipment (after goods are delivered and invoiced) |

| What's funded | Supplier costs to produce/ship goods | Outstanding invoices (accounts receivable) |

| Applies to | Tangible goods only | Goods and services |

| Common users | Manufacturers, distributors, importers | B2B businesses, staffing, transportation |

| Collateral | The confirmed purchase order | The issued invoice |

When to Use Both in Sequence

For large orders, using both products in sequence is often the strongest approach.

PO financing covers the upfront supplier payment. Once goods are delivered and invoiced, the same transaction can transition into invoice factoring — the factoring company advances cash against the receivable and pays down the PO financing balance first. This covers the full cycle from order receipt to cash collection.

Stirling Capital Group structures this kind of integrated arrangement, called a Trade Finance Facility, connecting clients with specialized lenders who can underwrite both phases as a single transaction — so there's no gap between fulfillment and getting paid.

Alternatives to Purchase Order Financing

If PO financing's cost or requirements don't fit your situation, three alternatives are worth considering:

Business lines of credit — revolving credit you can draw against for inventory or supplier costs. More flexible, lower cost (typically 7%–10% APR), but requires established business credit and may cap out at levels too low for large orders.

Invoice financing/factoring — useful after delivery when invoices exist. Can't solve the pre-shipment funding problem, but pairs well with PO financing.

Short-term business loans — lump-sum capital from banks or online lenders. Broader use of funds, but approval timelines and credit requirements vary significantly. SBA 7(a) working capital loans offer competitive rates but can take 5–10 business days for processing.

If you decide PO financing is the right fit, expect to find it through specialized online lenders and commercial finance companies. Traditional banks occasionally extend it to larger, established clients, but small and mid-sized businesses are more likely to find it through specialty finance sources.

This is where a commercial finance advisor earns their place in the process. Instead of approaching lenders one at a time and discovering their credit boxes don't fit, you evaluate multiple options at once. Stirling Capital Group maintains relationships with over sixty private lending sources — including specialty PO financing and supply chain finance lenders. For manufacturers, distributors, importers, and government contractors, that network means faster answers on whether PO financing, a business line of credit, or a combined structure fits a specific transaction.

Frequently Asked Questions

What is purchase order financing?

PO financing is a short-term cash advance where a lender pays your supplier directly to fulfill a confirmed customer order. You repay the advance once your customer settles the invoice, with no monthly payments in between.

What is an example of purchase order financing?

A clothing distributor receives a $300,000 wholesale order but can't pay their manufacturer. A PO financing company pays the manufacturer directly, the goods are delivered, the retailer pays the financing company, and the distributor keeps the profit minus financing fees.

How do you qualify for purchase order financing?

You must sell tangible goods to B2B or B2G customers, have creditworthy end customers, maintain gross margins above 20–25%, and present a confirmed purchase order with verifiable supplier documentation. Your own credit history is secondary.

What is a purchase order in finance?

A purchase order is a legally binding commercial document issued by a buyer confirming their intent to purchase specific goods at a set price. In PO financing, it serves as the primary collateral the lender evaluates.

What is the difference between PO financing and invoice factoring?

PO financing funds supplier costs before goods are shipped and before an invoice exists. Invoice factoring advances cash against invoices already issued after order fulfillment. Both tools serve cash flow needs — just at different points in the order cycle.

What are typical fees for purchase order financing?

Fees typically range from 1% to 6% of supplier costs per month. On a $100,000 advance at 2%/month over 60 days, that's $4,000 in fees, which annualizes to roughly 24% APR. Rates can reach 50%+ depending on the lender and deal structure.