Introduction

You've found the right commercial property — a value-add acquisition that fits your strategy precisely. The seller wants to close in 30 days. Your capital is tied up in an existing asset, and your bank needs 60 to 90 days just to begin underwriting.

This is the scenario bridge loans are built for.

Bridge loans solve a specific problem: speed. But how they actually work (the repayment structure, qualification criteria, and real costs) often surprises borrowers evaluating them for the first time.

This guide covers what a bridge loan is, how it works from application through repayment, when it makes sense to use one, what it costs, and what alternatives exist — so you can evaluate it clearly against your specific situation.

Key Takeaways

- Bridge loans are short-term financing (typically 6–36 months) secured by an existing asset to cover a capital need until a liquidity event closes

- They fund faster than conventional loans but carry higher interest rates and fees in exchange for that speed

- Qualification centers on collateral equity, credit profile, exit strategy, and cash flow — not income alone

- Common uses include commercial acquisitions, value-add real estate, and business transitions

- Private lenders and capital advisory firms step in when banks are too slow or decline the deal

What Is a Bridge Loan?

A bridge loan is a secured, short-term loan designed to "bridge the gap" between an immediate capital need and an anticipated future liquidity event — such as a property sale, a refinance into permanent financing, or the closing of a business transaction.

The OCC defines a commercial real estate bridge loan as short-term financing that allows newly constructed or acquired commercial properties to reach stabilization. That definition captures the core purpose: bridge loans carry a borrower, property, or acquisition from an interim state to a defined exit.

Why Bridge Loans Exist

Conventional financing — mortgages, SBA loans, bank term loans — typically takes 30 to 60 days to close after contract. Many commercial transactions run longer. When a deal carries a tight deadline, that timeline can eliminate traditional lenders from consideration entirely — making bridge financing the only viable path forward.

Bridge vs. Hard Money: A Quick Distinction

These terms overlap but aren't identical:

- Bridge loans cover a wider range of use cases — acquisitions, transitional assets, business transactions — and may come from banks, private lenders, or commercial finance firms

- Hard money loans are asset-based, sourced from private investors or groups, and used specifically for distressed or fix-and-flip properties where conventional lenders won't participate

In commercial real estate, the two terms are sometimes used interchangeably. The underlying structure is similar; the use case and lender type are what differ.

Two Primary Structures

| Structure | Who It Serves | Common Use |

|---|---|---|

| Residential | Homeowners | Buy a new property before the existing home sells; funds may come as a second mortgage or pay off the first to free up equity |

| Commercial & Investment | Businesses, developers, investors | Acquire or refinance during a transitional period — lease-up, renovation, value-add repositioning, or business acquisition — ahead of permanent financing |

How Does a Bridge Loan Work?

Bridge loans move fast — but the process is more structured than it looks. Here's how each stage works, from initial qualification through repayment.

Application and Pre-Qualification

The process starts when a borrower identifies the need — typically a pending deal with a closing deadline — and approaches a lender or commercial finance consultant to determine available loan amounts and terms.

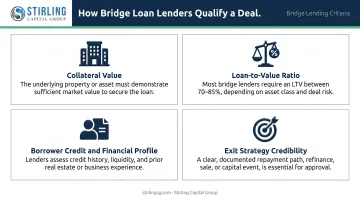

At this stage, lenders evaluate:

- Collateral value — the current market value of the asset being pledged

- Loan-to-value ratio — published lender sources commonly cap bridge leverage around 70% to 85%, depending on property type, completed value, and borrower profile

- Borrower credit and financial profile — sponsorship quality and demonstrated liquidity matter, not just a credit score

- Exit strategy credibility — how and when the bridge will be repaid is underwritten just as carefully as the loan itself

Many bridge transactions with private and non-bank lenders close in 30 days or less — a sharp contrast to the months-long process typical of conventional commercial loans.

Loan Structure and Disbursement

Once approved, the lender advances funds secured by the collateral asset to close the acquisition, fund a down payment, cover renovation costs, or meet another capital need.

Interest structure: Most bridge loans are interest-only during the loan term. The borrower pays interest monthly and repays the full principal in a lump sum — a balloon payment — at maturity. Some structures defer all payments until the exit event.

Typical terms:

| Feature | Common Range |

|---|---|

| Loan term | 6 to 36 months |

| Rates | Starting at 7.75%–9.49%+ (varies by lender) |

| Origination fees | 1.5%–3% of loan amount |

| LTV | 70%–85% depending on lender and asset type |

Rate and fee data are deal-specific. Current lender product pages typically advertise rate floors, not averages, so treat published ranges as starting points rather than market-wide benchmarks.

Repayment and Exit

The exit strategy is the most important element of any bridge loan. Repayment typically comes from one of three sources:

- Sale of the collateral or newly acquired asset

- Refinance into permanent long-term financing after stabilization

- Proceeds from a business transaction or capital event

You must define a realistic exit strategy before accepting the loan. If the anticipated sale or refinance is delayed, you carry both the bridge loan cost and any existing obligations simultaneously — which strains cash flow when timelines extend.

If the exit is delayed: Some lenders offer extensions. Kiavi, for example, advertises extensions of up to three months with a 1% fee on the unpaid principal balance.

In more severe situations, delays can result in the loan converting to an extended term structure or, in default, collection action against the collateral.

When and Where Are Bridge Loans Used?

Residential: Buying Before Selling

A homeowner finds a property they want to purchase before their existing home sells. A bridge loan unlocks the equity in the current home to fund the down payment — allowing the buyer to make a non-contingent offer and compete effectively in a fast-moving market without waiting on the sale to close first.

Commercial Real Estate

This is where bridge financing is most heavily used:

- Value-add acquisitions — buying a property that doesn't yet qualify for permanent financing due to low occupancy or deferred maintenance

- Lease-up transitional assets — funding the gap between construction completion and stabilized occupancy (JLL arranged $131.1M in bridge financing for a 390-unit luxury multifamily project in lease-up in 2025)

- Time-sensitive acquisitions — closing competitive deals when conventional lender timelines don't fit

Business Acquisitions and Transitions

Bridge loans also fund business acquisitions, equipment purchases, or operational capital needs while a borrower awaits an expected sale, refinance, or payout. For entrepreneurs and investors sitting on illiquid assets, bridge financing can be the difference between seizing an opportunity and watching it pass.

Where Bridge Financing Comes From

Traditional banks offer limited bridge products. Most commercial bridge transactions are funded by private lenders, institutional capital groups, or specialty finance firms — each with different appetite for collateral type, deal size, and timeline.

For borrowers who need fast, flexible capital, working with a commercial finance consultancy like Stirling Capital Group can cut weeks off the process. Rather than approaching lenders one at a time, Stirling draws on relationships with over 60 private lending sources to match borrowers with the right fit across fast-close acquisitions, transitional assets, land opportunities, and value-add commercial real estate throughout the continental United States.

Bridge Loan Costs, Pros & Cons

The Cost Structure

Bridge loans cost more than conventional financing. The total expense includes:

- Interest — Rate floors from published lenders start in the high single digits; actual pricing is deal-specific

- Origination fees — Typically 1.5%–3% of the loan amount, though current primary lender pages vary

- Appraisal, title, and closing costs — These apply to most secured real estate transactions and add to the total

- Extension fees — If the exit is delayed, extensions typically carry an additional cost (Kiavi's documented rate: 1% of unpaid principal balance per extension period)

That total cost must be weighed against the opportunity cost of not moving forward. A bridge loan's higher expense is often justified when the deal generates enough return — or when the alternative is losing a time-sensitive acquisition entirely.

Advantages

- Closes in days or weeks, not months

- No purchase contingency required on the new acquisition

- Flexible repayment structures, including interest-only and deferred options

- Provides capital access when traditional lending is too slow or unavailable

Risks

- Higher interest rates than conventional loans

- Carrying two debt obligations simultaneously during the bridge period

- Exposure if the exit event is delayed or proceeds fall short of projections

- Foreclosure on the collateral is a real risk in default scenarios — making a credible, realistic exit strategy essential before committing

Alternatives to Bridge Loans

Before committing to a bridge loan, evaluate whether one of these alternatives fits your situation more efficiently:

Home Equity Loan or HELOC

For residential borrowers with substantial equity, a HELOC may offer lower rates than a bridge loan — national average HELOC rates were approximately 7.43%–7.47% in June 2026. One caveat: some lenders won't issue a HELOC on a home already listed for sale.

Cash-Out Refinance

Replaces the existing mortgage with a larger one and delivers the difference in cash. Best suited when refinance rates are favorable and the borrower isn't under a tight closing deadline. U.S. Bank notes this process typically takes 30 to 45 days — workable in some scenarios, too slow in others.

Sale-Leaseback

In commercial contexts, a sale-leaseback allows a business to sell owned real estate to an investor while signing a long-term lease, retaining operational use of the property. This structure can unlock up to 100% of property equity with operational continuity maintained for 15 to 20 years or more — a viable alternative for businesses that need liquidity without short-term maturity risk.

Contingent Offer

In competitive real estate markets, a sale contingency is an option — but it weakens negotiating position considerably and isn't viable in competitive bidding situations.

The right alternative depends entirely on your timeline, equity position, and deal structure.

A quick comparison helps narrow the field:

| Alternative | Best For | Typical Timeline | Key Risk |

|---|---|---|---|

| HELOC | Residential equity access | 2–6 weeks | Unavailable on listed homes |

| Cash-Out Refinance | Rate-favorable environments | 30–45 days | Too slow for tight deadlines |

| Sale-Leaseback | Commercial liquidity needs | Varies by deal | Long-term lease commitment |

| Contingent Offer | Flexible seller negotiations | Depends on sale | Weakens offer competitiveness |

If none of these fit cleanly, a bridge loan may genuinely be the right tool — the goal is making that call deliberately, not by default.

Frequently Asked Questions

How does a bridge loan work?

A bridge loan is a short-term, secured loan that provides immediate capital — typically by borrowing against an existing asset — to fund a new purchase or capital need. Repayment is triggered by a future liquidity event such as a property sale or refinance into permanent financing.

How much would a $100,000 bridging loan cost?

Using a published lender rate floor of 9.49% (RCN Capital) on an interest-only structure, a $100,000 bridge loan would carry roughly $4,745 in interest over six months. Add origination fees of 1.5%–3% ($1,500–$3,000) and applicable closing costs, and total six-month carrying costs would likely fall in the $6,000–$8,000 range — though exact pricing varies by deal.

Are bridge loans hard to get?

Bridge loans have more flexible qualification criteria than conventional mortgages. Lenders focus primarily on collateral equity, a proven track record, and a credible exit strategy. Private and non-bank lenders are generally more accessible than traditional banks for these transactions.

How long does a bridge loan last?

Most bridge loans run 6 to 36 months. Six to 12 months is the most common term in residential transactions; 12 to 36 months is more typical for commercial real estate and investment property scenarios.

What is the difference between a bridge loan and a hard money loan?

Both are short-term, asset-secured loans — but hard money loans are typically used for distressed or fix-and-flip properties where conventional lenders won't participate. Bridge loans are broader in application and available from banks as well as private lenders; in commercial real estate, the two terms are often used interchangeably.

Can bridge loans be used for commercial properties or business acquisitions?

Yes. Bridge loans are widely used in commercial real estate for acquisitions, value-add projects, and transitional financing ahead of a permanent loan. They can also fund business acquisitions or operational needs when a borrower holds illiquid assets and a near-term liquidity event is in sight.