Asset-based lending (ABL) solves this by anchoring borrowing capacity to what a business owns, not just what it earns. According to the Secured Finance Network's 2025 Market Sizing Study, ABL commitments reached $537 billion at year-end 2024—a figure that reflects just how mainstream this financing tool has become.

This guide covers how ABL actually works: from collateral assessment and borrowing base mechanics through cash controls and ongoing monitoring—not just the definition.

Key Takeaways

- ABL is a loan or revolving credit line secured by business assets (receivables, inventory, equipment, real estate) rather than cash flow alone

- Borrowing capacity adjusts automatically as collateral values change — this dynamic limit is called the borrowing base

- Manufacturers, distributors, wholesalers, and seasonal businesses are the strongest candidates

- ABL typically carries fewer financial maintenance covenants than conventional loans but requires regular collateral reporting

- Businesses declined by traditional banks often qualify for ABL when their collateral base is strong

What Is Asset-Based Lending?

ABL is commercial financing where the loan amount and ongoing borrowing capacity are determined primarily by the appraised value of pledged business assets—not by EBITDA multiples or debt service coverage ratios that conventional lenders rely on.

The structure was built to solve a specific problem: many asset-rich businesses have balance sheets full of value but irregular free cash flow. Manufacturers waiting 60–90 days for customers to pay, distributors carrying large inventory positions, wholesalers managing seasonal demand—none of these qualify under traditional bank underwriting criteria, despite being fundamentally sound businesses.

What ABL is not matters just as much as what it is:

In factoring, the business sells receivables outright at a discount and transfers credit risk to the factor. ABL is different: assets are pledged as collateral, not sold, and the business retains ownership throughout.

- Merchant cash advances (MCAs) are short-term, high-cost products based on future revenue projections—not collateral quality.

- Personal asset loans operate against individual assets; ABL is structured at the commercial entity level against business assets.

Types of ABL Structures

Three primary ABL structures serve different business needs:

| Structure | Collateral Basis | Best For |

|---|---|---|

| Revolving line of credit | Accounts receivable, inventory | Working capital, seasonal businesses, growth |

| Term loan | Equipment, real estate | Capital expenditures, fixed-asset monetization |

| Hybrid / FILO | Multiple collateral types combined | Complex balance sheets, M&A, recapitalization |

The revolving facility is the most common ABL structure. Borrowing availability expands and contracts automatically as receivables and inventory levels change—creating a self-adjusting credit line that follows the business cycle rather than fighting it.

For businesses that don't fit a conventional bank's credit box, that flexibility is often the deciding factor.

How Does ABL Work?

ABL operates through four distinct stages: collateral assessment, borrowing base calculation, funding with cash controls, and ongoing monitoring. Each stage directly ties available credit to the quality and liquidity of pledged assets.

Collateral Assessment

Before any facility is approved, the lender conducts a field examination. Examiners review accounts receivable aging reports, payables, inventory records, and physical assets. Third-party appraisals are typically conducted for equipment, real estate, and inventory.

This stage determines eligible collateral—and not everything qualifies. Common exclusions include:

- Receivables past due by 90+ days (or 60 days past due date)

- Accounts where the customer can assert an offset or contra obligation

- Affiliate receivables and most foreign receivables

- Obsolete or specialized inventory with no active secondary market

- Customer concentrations above 10–20% of the borrowing base

- Equipment with significant legal encumbrances

The field exam is the lender's primary credit underwriting tool. It will be refreshed annually or semi-annually once the facility is in place.

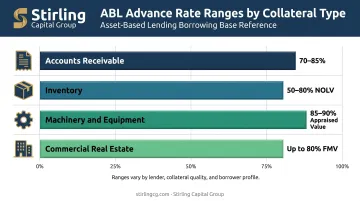

The Borrowing Base

The borrowing base is a calculated cap on how much the borrower can draw at any given time, expressed as an advance rate applied to eligible collateral. Typical advance rate ranges:

- Accounts receivable: 70–85% of eligible A/R (some lenders reach 85–90%)

- Inventory: 50–65% of book value, or up to 80% of Net Orderly Liquidation Value (NOLV)

- Machinery and equipment: 85–90% of appraised value

- Commercial real estate: generally up to 80% of fair market value

Note: These ranges vary by lender, collateral quality, industry, and borrower profile. They are representative ranges, not fixed benchmarks.

The borrowing base adjusts monthly—or weekly for larger facilities—as receivables are collected, new invoices are generated, and inventory turns over. As your asset base grows, so does your credit availability — and when collateral shrinks, the facility adjusts accordingly, keeping lender exposure tied directly to real-time business performance.

Funding and Cash Controls

Most ABL facilities include cash dominion provisions—arrangements where customer payments flow into a lender-controlled lockbox or blocked account that automatically sweeps against the outstanding loan balance. This keeps the facility current and frees up new borrowing capacity as receivables are collected.

There are two versions:

- Hard dominion: Lender control over collections is always in effect, regardless of availability or covenant status

- Springing dominion: Cash remains freely available to the borrower until a trigger event (such as a covenant breach or low availability threshold) activates lender control

Springing structures give the borrower more day-to-day operational flexibility. Hard dominion is more common in higher-risk or larger facilities where lenders require tighter ongoing control. Either way, how a borrower manages cash flow connects directly to the reporting obligations that govern the facility day to day.

Ongoing Monitoring and Reporting

The Borrowing Base Certificate (BBC) is the operational heartbeat of any ABL facility. Borrowers submit a BBC monthly (or weekly for larger or riskier facilities) that updates:

- Current receivables aging and eligible balances

- Inventory totals and any write-downs or ineligibles

- Calculated borrowing availability

The BBC is how the lender determines the live credit limit at any given moment. Missing or inaccurate certificates can trigger a default or reduce availability—making internal accounting discipline an operational priority.

Who Should Consider ABL?

The strongest ABL candidates share a common profile: asset-heavy balance sheets with uneven or cyclical cash flow. Specific business types include:

- Manufacturers bridging the gap between raw material purchases and customer payment

- Distributors and wholesalers managing large inventory positions against receivable cycles

- Seasonal retailers with pronounced demand swings requiring flexible liquidity

- Importers and government contractors facing extended payment cycles

- Rapidly growing companies whose receivables and inventory are outpacing their conventional credit lines

- Businesses in M&A, leveraged buyouts, or restructuring where conventional lending is unavailable due to elevated leverage or earnings disruption

Companies declined by conventional banks due to leverage ratios, earnings variability, or limited operating history are often strong ABL candidates. The primary underwriting lens is collateral quality, not profitability metrics.

That said, finding the right ABL structure is rarely straightforward. Advance rates, eligibility criteria, covenant packages, and reporting requirements vary significantly across lenders. Stirling Capital Group maintains relationships with more than 60 specialized private lending sources across multiple collateral types—including bank ABL groups, non-bank asset-based lenders, private credit funds, and turnaround specialists—allowing businesses to compare options across lenders rather than fitting into a single institution's credit box.

Benefits and Risks of ABL

Key Advantages

- Higher borrowing limits than unsecured credit, tied directly to asset value rather than a fixed credit score threshold

- Covenant-light structure — Bank of America notes that ABL typically involves fewer restrictive financial maintenance covenants than traditional business financing

- Scalable credit — availability grows as the business grows its receivables and inventory, without renegotiating the facility

- Accessible for non-traditional borrowers — collateral-driven underwriting opens doors for businesses that don't qualify on cash flow metrics alone

- Strong historical recovery — SFNet's comment letter reports a 98% recovery rate for ABL facilities over a 12.5-year period through October 2020

Primary Risks

- Reporting burden: Borrowing Base Certificates, field exams, and collateral audits add meaningful administrative overhead—especially for companies without robust accounting systems

- Collateral volatility: A drop in receivable quality, inventory write-downs, or customer concentration issues can reduce available credit unexpectedly and quickly

- Lender control: Cash dominion arrangements—particularly hard dominion—give lenders significant influence over cash management. In a default scenario, the lender has the right to seize and liquidate pledged assets

- Complexity at setup: Multi-collateral facilities involving receivables, inventory, and equipment require more structuring work upfront than a conventional term loan

Understanding these risks puts the ABL-vs.-cash-flow decision in sharper focus. Cash-flow lending suits businesses with stable, predictable earnings and minimal reporting appetite. ABL fits businesses with strong assets but earnings variability. The right choice depends on where most of the company's value lives—on the income statement or the balance sheet.

Conclusion

ABL's core logic is straightforward: borrowing capacity follows what a business owns, not just what it earns. For asset-rich companies navigating growth, seasonality, or periods where conventional financing falls short, that distinction can open financing options that a P&L alone would never qualify for.

Understanding the mechanics puts business owners in a stronger position when evaluating whether ABL fits their situation:

- Borrowing base calculations determine how much availability a business can actually draw

- Field exams establish which collateral is eligible and at what advance rate

- Cash dominion structures affect how daily cash flow is swept and applied

That working knowledge shapes both lender selection and how a deal gets structured around an actual operating cycle.

For business owners ready to explore ABL options, Stirling Capital Group offers a free consultation and access to a curated network of more than 60 private lending sources. The advisory process covers lender identification, deal structuring, and full execution support from first conversation through close. Reach the team at info@stirlingcg.com or 614-470-4716.

Frequently Asked Questions

Can I get a loan based on my assets?

Yes. Asset-based lending allows businesses to borrow against assets like accounts receivable, inventory, and equipment, with the loan amount tied to the appraised value of eligible collateral. Credit score and cash flow still factor in, but collateral quality is the primary underwriting driver.

What is an example of an asset-based loan?

A manufacturer with $2 million in outstanding invoices might qualify for a revolving ABL line up to 75–85% of eligible receivables. As customers pay invoices and new ones are generated, the borrower draws and repays continuously, keeping working capital fluid across the full production and collection cycle.

What is the difference between asset-based lending and cash flow lending?

Cash-flow lending qualifies borrowers based on EBITDA and leverage ratios. ABL bases borrowing capacity on the value of pledged assets. A business with strong receivables and inventory but inconsistent earnings will often qualify for ABL when a traditional cash-flow loan is out of reach.

What assets can be used as collateral in an ABL facility?

The most common are accounts receivable (highest advance rates, most liquid), inventory, machinery and equipment, and commercial real estate. Not every asset qualifies. Lenders assess liquidity, marketability, and likely recovery value before including an asset in the borrowing base.

Can you buy a house with an SBLOC?

An SBLOC (Securities-Based Line of Credit) is a personal finance product that uses an investment portfolio as collateral—it is a separate product from commercial ABL. Most SBLOC agreements prohibit using proceeds to purchase or trade securities. Real estate purchase restrictions vary by lender agreement, and SBLOCs are generally not structured for that purpose.