Introduction

You've built a successful business. You own the building you operate from — a real asset worth millions — but your working capital is stretched thin and growth opportunities are slipping by. The capital you need is sitting right there on your balance sheet, locked inside four walls you can't easily touch.

A sale-leaseback resolves exactly that tension. The structure lets a business sell an owned asset — most commonly commercial real estate — to an investor and immediately lease it back, staying fully operational while converting illiquid equity into usable cash.

It's neither a traditional loan nor equity financing, which makes it a flexible tool for businesses that need capital without taking on new debt or giving up ownership stakes.

This article explains how a sale-leaseback works mechanically, who benefits most from the structure, real-world examples from recognizable companies, and the key risks worth understanding before moving forward.

Key Takeaways

- A sale-leaseback converts owned assets into immediate cash while preserving full operational use of those assets.

- It releases 100% of an asset's market value — compared to traditional secured lending, which advances only a portion.

- Lease payments are fully tax-deductible in a qualifying true sale structure.

- Under ASC 842, most sale-leaseback obligations appear on the balance sheet as a right-of-use asset and lease liability.

- IRS reclassification risk and existing debt covenant restrictions are the two most critical diligence items to resolve before structuring a deal.

What Is a Sale-Leaseback?

A sale-leaseback is a financial transaction in which an asset owner sells a property or piece of equipment to a buyer and simultaneously signs a lease agreement to continue using that asset. Ownership transfers to the buyer, but the seller's day-to-day operations continue uninterrupted.

The Two Parties and Their Roles

The transaction involves two counterparties with distinct, complementary roles:

- Seller/Lessee — The original owner sells the asset and becomes the tenant, paying rent while retaining full use of the space or equipment.

- Buyer/Lessor — The investor acquires the asset, holds title, and collects rent as the new landlord.

The seller surrenders ownership but retains operational control. The buyer acquires an income-producing asset with a tenant already in place — no lease-up period required.

Why It's Considered a Hybrid Financing Tool

Sale-leasebacks sit between debt and equity on the capital structure spectrum. Unlike a loan, the proceeds don't create traditional debt on the balance sheet. Unlike equity financing, the transaction doesn't dilute ownership. Investopedia characterizes sale-leasebacks as a hybrid debt product that can provide capital without increasing a company's debt load or requiring equity financing. That said, current accounting standards (ASC 842) mean most lease obligations do appear on the balance sheet in some form.

What Assets Qualify?

The most common asset class is commercial real estate — offices, warehouses, manufacturing facilities, and retail locations. But sale-leasebacks also apply to:

- Industrial and manufacturing equipment

- Aircraft and fleet vehicles

- Construction machinery

- Any high-value, fixed asset with a clear market value

How a Sale-Leaseback Transaction Works

The mechanics are straightforward, though the legal and accounting details require careful handling.

Step-by-Step Transaction Flow

- The business identifies a qualifying asset it owns outright or with sufficient equity.

- A buyer or investor is sourced — typically a commercial real estate investor, REIT, or institutional fund.

- The asset is sold at or near fair market value, with proceeds delivered to the seller at closing.

- A lease agreement is signed simultaneously, establishing the rent, term, and operational conditions.

- The business continues operating from the same location, now as a tenant rather than an owner.

Lease Structure and Financial Attractiveness

Lease payments in a sale-leaseback are typically negotiated to reflect an implied cost of capital tied to the property's capitalization rate. According to Plante Moran, the cap rate effectively functions as the cost of capital for that financing source — making the rate comparison to traditional lending a deal-specific calculation rather than a standard benchmark.

End-of-Lease Options

Lease terms commonly run from several years to multiple decades. At lease end, the lessee typically has options to:

- Renew the lease for an additional term

- Vacate the property if operations have changed

- Repurchase the asset — though this last option carries significant risk

A repurchase option is a structural red flag. PwC notes that a repurchase option generally precludes sale accounting under ASC 842 unless it is at then-prevailing fair value and substantially similar alternative assets are readily available — a bar that's difficult to clear for unique commercial properties.

Accounting Treatment Under ASC 842

The legacy framing of sale-leasebacks as off-balance-sheet transactions is largely outdated. Under FASB ASU 2016-02, lessees must recognize a right-of-use asset and a lease liability for both finance and operating leases, with limited exceptions for short-term leases.

The effective date was fiscal years beginning after December 15, 2018 for public companies. Many private companies followed for fiscal years beginning after December 15, 2021.

Practical example: A manufacturing company owns its facility, valued at $5 million. It sells to a commercial real estate investor, receives $5 million in cash at closing, and signs a 15-year lease at a fixed monthly rent. The company stays in its building, redirects the $5 million into equipment upgrades and working capital, and pays rent instead of carrying property on its balance sheet.

Consult an accounting professional to understand how lease classification affects your specific financial statements.

Key Benefits of a Sale-Leaseback

Seller/Lessee Benefits

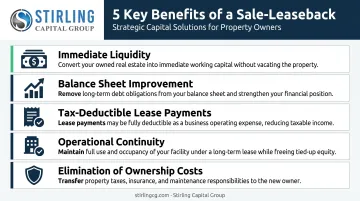

- Immediate liquidity without new debt — a sale-leaseback can release 100% of a property's market value, according to Plante Moran. Traditional secured lending typically advances only a fraction of appraised value; the sale-leaseback delivers cash, not credit.

- Balance sheet improvement — the transaction removes a fixed asset and replaces it with cash. Depending on structure and lease classification, it can improve leverage ratios and debt capacity, making the business more attractive to future lenders.

- Tax deductibility of lease payments — in a properly structured true sale-leaseback, all rent payments are deductible as ordinary business expenses. This contrasts with a traditional mortgage, where only the interest portion qualifies. Tax treatment depends on whether the IRS treats the arrangement as a genuine lease — professional tax advice before closing is essential.

- Operational continuity — nothing changes on the ground. Employees, customers, and workflows are unaffected; the business keeps its space and simply pays rent instead of holding title.

- Elimination of ownership costs — under a net lease structure, the business transfers responsibility for property taxes, maintenance, and insurance to the new owner.

Buyer/Lessor Benefits

- Predictable income stream — the buyer acquires a property with a creditworthy, long-term tenant already in place, removing lease-up risk.

- Net lease structures — buyers often negotiate net leases, where tenants pay rent plus specified property expenses, improving landlord economics.

- Asset appreciation potential — the buyer holds title to tangible real estate that may appreciate over time.

Common Industries and Real-World Examples

Who Uses Sale-Leasebacks Most?

Capital-intensive industries with high-value fixed assets are the most active users:

- Commercial real estate (office, industrial, retail)

- Manufacturing and heavy equipment

- Aviation — airlines regularly monetize aircraft to free operational capital

- Transportation and logistics — fleet vehicle sale-leasebacks

- Retail chains — selling store locations to REITs and leasing back on long-term net leases

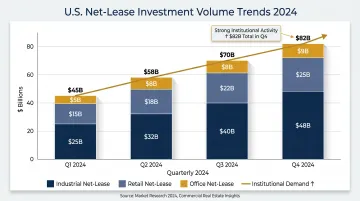

Industrial and logistics assets dominated net-lease investment activity in Q4 2024, representing 64% of transaction volume, according to CBRE's net-lease market data.

Real-World Examples

Red Robin (Restaurant/Retail): In March 2024, Red Robin completed its third sale-leaseback transaction, generating approximately $24 million in gross proceeds from 10 owned restaurant properties. The capital was deployed toward the company's broader financial strategy while all locations remained fully operational.

SAS Airlines (Aviation): In March 2023, Reuters reported that SAS entered sale-leaseback agreements with Aviation Capital Group covering 10 Airbus A320neo aircraft — converting high-value aircraft into liquidity while keeping every plane in service.

2024 Net-Lease Market: What the Data Shows

CBRE reported $43.7 billion in U.S. net-lease investment volume in 2024, up 13% year over year, with Q4 2024 alone reaching $13.7 billion — a 57% year-over-year surge. This reflects the broader net-lease market, not sale-leaseback volume alone. Even so, it signals strong institutional appetite for the tenanted assets that sale-leaseback transactions produce.

Potential Risks and Key Considerations

Loss of Ownership and Future Appreciation

Once the sale closes, the seller no longer benefits from property appreciation. If the asset's value rises significantly over the lease term, the seller/lessee pays rent on a property worth far more than the original sale price, which can represent a substantial opportunity cost in rising real estate markets.

IRS Reclassification Risk

The IRS may recharacterize a sale-leaseback as a disguised financing arrangement rather than a true sale if certain factors are present. IRS Written Determination 2001-0072, citing Revenue Ruling 55-540, identifies qualitative factors including:

- Lease payments that build lessee equity over time

- A nominal purchase option that makes title transfer virtually certain

- Payments materially above fair rental value

- Interest-equivalent payment structures

If reclassified, rent payments lose their full deductibility — only an interest equivalent would be deductible, and the seller would still be treated as the owner for tax purposes. Qualified tax counsel should review the structure before any agreement is executed.

Debt Covenant Restrictions

Businesses with existing credit facilities need to review their loan agreements carefully. As Cleary Gottlieb notes, debt agreements commonly restrict sale-leasebacks through asset sale covenants, lien restrictions, and investment limitations. A sale-leaseback could trigger:

- Mandatory prepayment obligations

- Lien capacity restrictions affecting the leaseback obligation

- Technical defaults under existing credit agreements

Leveraged companies especially should complete legal review before proceeding.

Is a Sale-Leaseback Right for Your Business?

A sale-leaseback makes the most strategic sense for businesses in specific situations:

- Need growth capital but can't qualify for traditional loans — the transaction bypasses conventional bank credit requirements entirely

- Carrying high-interest debt — sale proceeds can pay down expensive obligations, improving credit metrics and WACC

- Planning an exit or recapitalization — unlocking real estate equity before a sale can improve balance sheet optics and make the business more attractive to acquirers

- Facing cash flow pressure — access to operational capital without disrupting the business itself

- Expanding into new markets — freeing capital from owned properties to fund new locations or acquisitions

If your situation aligns with one or more of those scenarios, execution is the next challenge. Finding a qualified buyer and negotiating favorable lease terms are where most deals succeed or stall. Stirling Capital Group connects business owners with CRE investors and institutional buyers who specialize in sale-leaseback acquisitions — drawing on a network of over 60 private lending and investment sources. The advisory process covers buyer identification, transaction structuring, and coordination with legal and tax professionals from first call through closing.

A free consultation is available to assess whether your property and capital objectives align with a sale-leaseback structure. Reach the team at 614-470-4716 or info@stirlingcg.com.

Frequently Asked Questions

Why would a company do a sale and leaseback?

The primary motivations are unlocking capital tied up in fixed assets, improving liquidity, funding growth or debt paydown, and accessing more proceeds than traditional secured lending would allow — all without losing operational use of the asset.

What types of assets can be used in a sale-leaseback?

Commercial real estate — offices, warehouses, factories — is the most common. Sale-leasebacks also apply to aircraft, fleet vehicles, manufacturing equipment, and other high-value fixed assets with a clear market value.

What is the difference between a sale-leaseback and a traditional mortgage?

A mortgage is a loan secured by the asset; the business retains ownership but takes on debt. A sale-leaseback transfers ownership entirely in exchange for cash, so the business loses title but gains more capital and pays rent instead of debt service.

What are the tax implications of a sale-leaseback?

In a properly structured true sale-leaseback, all lease payments are fully deductible as business expenses. If the IRS reclassifies the transaction as financing, only an interest equivalent is deductible.

Is a sale-leaseback considered debt on the balance sheet?

Under ASC 842, most sale-leaseback obligations are recorded as a right-of-use asset and lease liability. The exact treatment depends on lease classification, term length, and how the transaction is structured under current GAAP.

Who typically buys assets in a sale-leaseback transaction?

Common buyers include institutional investors, REITs, private equity firms, commercial real estate investors, and specialty finance companies. These buyers seek stable, long-term income from creditworthy tenants with existing operating businesses.