Direct lending exists precisely to fill that gap. Non-bank lenders — private credit funds, business development companies, specialty finance groups — provide financing directly to companies without the intermediaries, committee layers, and standardized credit boxes that define conventional bank lending.

This guide breaks down what direct lending is, how it works from a borrower's perspective, how it compares to bank financing, what it costs, and how businesses can access it.

Key Takeaways

- Direct lending now accounts for 52% of total private credit AUM — it's the dominant private credit strategy, not a niche alternative

- Loans are typically floating-rate, senior secured, and privately negotiated with flexible structures

- Direct lenders underwrite each deal individually, making them viable for borrowers banks routinely decline

- Speed is a core advantage — transactions can close in weeks rather than months

- Higher cost is the trade-off — direct lending carries a spread premium over traditional bank and broadly syndicated loans

What Is Direct Lending?

Direct lending is a form of private credit where non-bank lenders provide loans directly to companies, bypassing banks and syndicated loan markets entirely. The result: privately negotiated, customized financing arranged directly between lender and borrower.

The market grew substantially after the Global Financial Crisis. As banking regulations tightened post-2008, banks pulled back from leveraged lending and riskier borrowers, creating a funding gap that private and institutional lenders moved to fill. Direct lending's share of middle-market LBO issuance rose from 36% in 2014 to 84% in 2023, while syndicated debt dropped from 64% to 16% over the same period.

Today, direct lending is the largest sub-strategy within private credit. U.S. direct lending AUM reached $751 billion as of June 2023, up from just $43.5 billion in December 2009 — and Preqin projects continued growth to $1.4 trillion by year-end 2028.

What Types of Loans Fall Under Direct Lending?

Direct lending encompasses several distinct loan structures, each sitting at a different position in a borrower's capital stack:

- First-lien senior secured loans carry the highest repayment priority: if the borrower defaults, first-lien holders are paid before anyone else. This is the most common direct lending structure.

- Second-lien loans are secured by the same collateral but sit lower in the repayment waterfall. Lenders accept more risk; borrowers pay a higher rate.

- Unitranche facilities blend senior and subordinated debt into a single loan, simplifying the capital structure for the borrower. U.S. middle-market unitranche issuance hit $210 billion in 2024, up from $94 billion the prior year.

- Mezzanine debt sits below senior facilities and often carries equity-linked economics — warrants or conversion features that compensate lenders for the added subordination risk. It's common in real estate development and leveraged buyouts where senior debt alone falls short.

Choosing between these structures comes down to three variables: how much debt the business can support, where a lender is willing to sit in the capital stack, and what rate the borrower can absorb.

How Direct Lending Works: A Step-by-Step Look

Origination and Approach

A business identifies a capital need — an acquisition, expansion, recapitalization, or refinancing — and approaches a private credit manager, business development company (BDC), or a commercial finance intermediary. Unlike a bank application, this enters a bilateral negotiation rather than a standardized credit process.

Working through an intermediary like Stirling Capital Group means the borrower's situation is pre-qualified and pre-underwritten before any lender is formally engaged — which sharply reduces wasted time and the cost of misaligned submissions.

Underwriting and Due Diligence

Direct lenders evaluate the borrower's cash flows, EBITDA, enterprise value, collateral, and overall capital structure. Morgan Stanley places middle-market direct lending borrowers at companies with $10 million to $250 million in EBITDA, though individual lenders set their own thresholds.

The underwriting is more hands-on than a bank's standardized scorecard — and more customized. That said, it requires the borrower to come prepared. Expect to provide:

- 2–3 years of profit and loss statements and balance sheets

- A business overview or confidential information memorandum (CIM)

- Current financial projections

- A clear explanation of the capital need and use of proceeds

Deal Structuring

Lender and borrower negotiate key terms including:

- Loan amount and draw structure

- Interest rate (floating, benchmarked to SOFR)

- Covenant package (maintenance vs. incurrence covenants)

- Collateral requirements and security interest

- Maturity date and any prepayment provisions

- Equity co-investment components, if applicable

This negotiability is one of direct lending's defining advantages. Unitranche structures, PIK toggle options, and delayed-draw facilities are all on the table. A conventional bank product offers none of these.

Timeline and Speed

Direct lending transactions can often close in a matter of weeks. That's a meaningful contrast to traditional bank credit committee processes, which routinely stretch to 60–90+ days. For time-sensitive acquisitions or competitive deal situations, that speed difference can determine whether a borrower wins or loses the opportunity outright.

Ongoing Lender Relationship

After closing, direct lenders maintain regular contact with borrowers, monitoring financial performance throughout the loan term. This ongoing relationship works in the borrower's favor: if business conditions change, direct lenders are far more willing to engage in covenant amendments or restructuring discussions than a conventional bank. That flexibility is often what keeps a temporary setback from becoming a permanent problem.

Key Features of Direct Lending Loans

Direct loans carry several structural characteristics that affect cash flow, covenant compliance, and strategic flexibility. Here's what borrowers need to know before signing.

Floating-rate structure: The Federal Reserve notes that almost all private credit loans are floating rate, benchmarked to SOFR (which replaced LIBOR when all USD LIBOR panel settings ceased on June 30, 2023). Your interest payments move with market rates.

In a falling-rate environment, that's a benefit. In a rising-rate environment, it can strain cash flow. Borrowers should model interest rate sensitivity carefully before signing.

Private and confidential: Unlike public bond issuances that require regulatory filings and broad market disclosure, direct lending agreements are privately negotiated. Sensitive business information, competitive positioning, and financial details stay out of the public domain.

Covenant structures — two types borrowers must understand:

- Maintenance covenants require ongoing financial tests — leverage ratios, interest coverage minimums — typically measured quarterly. Missing a threshold is an event of default, giving lenders rights to accelerate or enforce.

- Incurrence covenants activate only when the borrower takes a specific action, such as issuing new debt or making an acquisition. Less burdensome day-to-day, but they cap strategic flexibility.

Of the two, maintenance covenants appear far more consistently in direct lending than in broadly syndicated loan markets. That consistency carries an upside — it creates an early-warning dialogue. If the business hits a rough patch, lenders are alerted early enough to negotiate a solution rather than react to a crisis.

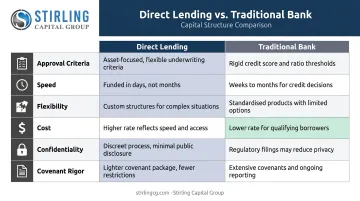

Direct Lending vs. Traditional Bank Financing

| Factor | Direct Lending | Traditional Bank |

|---|---|---|

| Approval criteria | Individually underwritten; evaluates cash flow, collateral, enterprise value | Standardized credit box; strict requirements on leverage, coverage, credit score |

| Speed | Weeks to close | 60–90+ days typical |

| Flexibility | Unitranche, PIK, delayed-draw, equity co-investment | Standardized products |

| Cost | Higher — spread premium over bank and BSL rates | Lower baseline rate |

| Confidentiality | Privately negotiated | Subject to regulatory review |

| Covenant rigor | Maintenance covenants standard | Varies; often less frequent testing |

On cost: Morgan Stanley reports that 2025 direct lending spreads on LBO loans averaged 153 basis points above broadly syndicated loan spreads. That premium is real, and borrowers should account for it. But context matters — many borrowers simply cannot access bank financing at all, making the rate comparison somewhat theoretical.

That access gap shows up in the data. Banks' share of LBO loans to private equity borrowers dropped to just 7% in 2023, according to Morgan Stanley — a clear signal that for complex deals, direct lending has become the primary path forward, not a backup option.

Benefits and Risks of Direct Lending for Borrowers

Benefits of Direct Lending

Access for underserved borrowers. The U.S. middle market includes nearly 200,000 businesses representing roughly one-third of private-sector GDP. Many of these companies are too small for public debt markets and too complex for conventional bank financing. Direct lending was built for them.

Speed as a competitive weapon. When you're competing for an acquisition target against a bank-financed buyer, closing in weeks rather than months can determine who wins the deal.

Relationship-based flexibility. Direct lenders who monitor borrower performance closely are positioned to engage constructively when conditions change. Lincoln International reported that amendment activity increased 13% quarter-over-quarter in recent quarters — evidence that lenders are actively working with borrowers rather than immediately enforcing defaults.

Risks and Considerations for Borrowers

Direct lending comes with trade-offs borrowers need to model before committing:

- Floating-rate exposure: When base rates rise, so does your debt service. The Federal Reserve has noted that private credit borrowers' average interest coverage ratio has declined to approximately 2.0x — a warning sign that rising rates are already compressing capacity. Run rate scenarios before signing.

- Covenant compliance burden: Maintenance covenants require ongoing financial reporting and adherence to defined ratios. The covenant default rate in private credit stood at 3.2% as of Q3 2025 (Lincoln International) — manageable, but a real operational commitment from day one.

- Qualification threshold: Direct lenders require demonstrable cash flows, enterprise value, and a credible capital structure. Businesses that cannot articulate a clear repayment path will struggle to qualify.

How Businesses Can Access Direct Lending

Two main paths exist for borrowers seeking direct lending:

Approaching private credit managers or BDCs directly — BDCs are regulated closed-end investment companies created under the Investment Company Act of 1940 that primarily provide senior secured, floating-rate financing to middle-market businesses. This route typically requires existing institutional relationships.

Working through a commercial finance intermediary — An advisory firm with established lender relationships can pre-qualify, pre-underwrite, and match the borrower to appropriate lenders across multiple institutions simultaneously. For most middle-market borrowers and entrepreneurs, this is the faster and more practical route.

Stirling Capital Group, a Columbus, Ohio-based commercial finance consultancy, operates in this capacity. With access to over 60 private lending sources — including private credit funds, senior secured lenders, specialty finance providers, and turnaround lenders — Stirling structures and places financing on behalf of borrowers across the continental U.S., major Canadian cities, and Puerto Rico.

The practical difference between approaching a single lender versus working with an intermediary like Stirling comes down to optionality. A single lender offers one credit box.

Stirling's network spans multiple lenders across every major category of commercial finance, each with different:

- Industry preferences and risk tolerances

- Advance rate structures and collateral requirements

- Deal size appetites and geographic focus

Rather than a binary approval-or-rejection outcome, borrowers get competitive financing options and the structuring expertise to identify which solution genuinely fits their situation.

Borrowers engaging Stirling should expect a free initial consultation covering the capital need, collateral profile, capital structure, and strategic objectives — followed by pre-underwriting and lender matching before any formal submission.

Frequently Asked Questions

Is direct lending a good idea?

Direct lending is a strong option for businesses that need flexible, fast, or customized capital that traditional banks won't or can't provide. The trade-off is clear: higher cost and covenant obligations. If your business qualifies and the speed or structure justifies the premium, it's often the most practical path to capital.

What is an example of direct lending?

A mid-sized company secures a unitranche loan from a private credit fund to finance a competitor acquisition. The deal closes in weeks through bilateral negotiation — no bank committee, no syndication, no public market process. The borrower gets speed and certainty; the lender gets a negotiated rate and covenant package.

How is direct lending different from a traditional bank loan?

Direct lenders underwrite each deal individually rather than applying standardized credit criteria, move faster, and offer more flexible structures — but charge higher interest rates. Banks are cheaper when they'll lend to you; direct lenders exist for situations where banks won't or can't.

Who qualifies for direct lending?

Direct lending is typically targeted at private middle-market companies with demonstrable cash flows and enterprise value — businesses pursuing acquisitions, refinancings, or growth capital, as well as real estate investors and owner-operators who fall outside bank lending parameters.

What types of loans are available through direct lending?

Common structures include senior secured first-lien loans, second-lien loans, unitranche facilities, and mezzanine debt. The right choice depends on the borrower's capital needs, risk profile, and position in the capital stack.

How long does it take to close a direct loan?

Direct lending transactions often close in weeks rather than the months typical of traditional bank financing. The timeline varies based on deal complexity, borrower preparation, and lender availability.