Introduction

An investor spots a distressed commercial property at a price well below market value. The seller wants to close in ten days. A conventional bank, working through its standard 33–39 day approval process, simply can't move that fast. This is exactly the scenario where a hard money lender becomes the decisive financing tool.

That scenario plays out across more deal types than most borrowers expect. Real estate investors, commercial buyers, and entrepreneurs pursuing time-sensitive acquisitions all rely on hard money loans when traditional financing is unavailable or too slow — not just house flippers. This guide breaks down what hard money lenders are, how their loans work, what they cost, and what to look for before you commit.

Key Takeaways

- Hard money loans are short-term, asset-backed loans from private lenders — approval hinges on the property's value, not the borrower's credit score

- Interest rates typically range from 9%–15%, compared to 6–8% for conventional mortgages, with loan terms of 6–24 months

- Best suited for fix-and-flip projects, distressed acquisitions, and commercial real estate where traditional financing is too slow or unavailable

- Down payments generally range from 20%–40%, with loan amounts capped at 60%–75% of the property's current value or ARV

- Compare lenders across rates, fees, terms, and deal-type experience before committing

What Is a Hard Money Lender?

A hard money lender is a private individual, investment company, or specialty finance firm — not a bank or credit union — that provides short-term loans secured by real estate. The term "hard" refers to the hard asset (the property) used as collateral, not the difficulty of obtaining the loan.

In practice, hard money lenders include private investors, private equity groups, lending funds, and specialty finance companies. Because they aren't regulated the same way as traditional banks, they have far more flexibility to set their own underwriting criteria and move quickly.

The Core Distinction from Traditional Lending

Conventional lenders evaluate borrowers based on credit history, income documentation, and debt-to-income ratios. Hard money lenders do the opposite — their primary question is whether the property's value is sufficient to recover their principal if the borrower defaults. This makes hard money accessible to borrowers who can't qualify conventionally, including those with:

- Complex income documentation or self-employment

- Recent credit events

- Properties in poor condition that banks won't touch

- Non-conforming deal structures

Common Use Cases

- Fix-and-flip projects — purchase and renovate for resale

- BRRRR strategy — buy, rehab, rent, refinance, repeat

- Time-sensitive acquisitions — auction purchases, off-market deals

- Commercial real estate — retail, industrial, mixed-use assets

- Distressed properties — rehabilitation candidates that fall outside conventional underwriting

These use cases sometimes overlap with bridge lending, which is worth clarifying. Hard money and bridge loans are often used interchangeably — but the terms aren't identical. Bridge loans typically describe financing for transitional commercial or income-producing properties. Hard money most often applies to renovation-focused investing or deals that fall outside bank underwriting guidelines entirely.

How Hard Money Loans Work

The Asset-Based Underwriting Model

Hard money lenders use three primary metrics to determine how much they'll lend:

| Metric | What It Measures | Typical Cap |

|---|---|---|

| LTV (Loan-to-Value) | Loan vs. current "as-is" property value | 50%–75% |

| ARV (After-Repair Value) | Projected value post-renovation | 65%–70% of ARV |

| LTC (Loan-to-Cost) | Loan vs. total project cost (purchase + rehab) | Varies by lender |

An unrealistic ARV estimate or a thin margin between all-in cost and ARV will stop approval regardless of how strong the borrower's profile is.

The Step-by-Step Process

- Deal submission — Borrower provides property details, purchase price, rehab scope, and exit strategy

- Lender analysis — Lender orders a BPO or appraisal and reviews deal fundamentals

- Term sheet issued — Rate, points, fees, and loan amount are proposed

- Closing — Often within days to a few weeks, depending on appraisal timing

- Draw releases — For renovation loans, rehab funds are released in staged tranches as work is completed and inspected

How Draw Schedules Work

Renovation funds are not disbursed in a lump sum. They're held in reserve after closing and released as milestones are met — only after independent inspectors confirm that line items are 100% complete, not just in progress.

Each draw typically requires a third-party inspection report and photos before funds are released. Budget for inspection fees at each draw stage; delays in approvals can affect project timelines and cash flow.

Exit Strategy and Loan Structure

Managing draw timelines well matters — but none of it counts if the loan lacks a credible exit plan. Lenders evaluate this before approving anything. The two most common exits are:

- Sell the renovated property and repay from sale proceeds

- Refinance into a conventional mortgage or DSCR loan for rental hold

A vague or speculative exit strategy signals deal risk to lenders, and it creates real exposure for borrowers if market conditions shift mid-project.

Most hard money loans are structured as interest-only during the loan term, with full principal repaid in a balloon payment at maturity. Loan terms typically run 6–24 months. If the project runs long, extension fees apply — and some lenders don't offer extensions at all, making realistic timeline planning essential from the start.

Hard Money Loan Requirements

Borrower Requirements

Credit score requirements vary widely. Some hard money lenders have no formal minimum; others set floors around 600–650. Lenders like Kiavi require 640 while others like Easy Street Capital accept 600. The deal's strength matters far more than the credit score.

Key borrower factors lenders evaluate:

- Deal strength — the spread between all-in cost and ARV

- Investing experience — first-time investors typically face more conservative terms

- Liquidity and reserves — cash available for carrying costs, delays, and unexpected expenses

- Exit strategy credibility — a realistic and executable plan to repay

First-time investors should expect higher equity requirements and more conservative leverage until they establish a track record. The financial thresholds below reflect what most lenders look for once they move past the credit check.

Typical financial requirements:

- Down payment: 20%–40%, depending on lender, deal strength, and borrower experience

- Higher leverage: Available to experienced investors with strong ARV spreads

- Cash reserves: Sufficient to cover carrying costs, delays, and unexpected expenses — even when income documentation isn't required

Property Requirements

Hard money lenders are generally flexible on property condition — this is one of their core advantages over conventional lenders. Eligible property types commonly include:

- Single-family investment properties

- Multi-family residential

- Fix-and-flip projects

- Commercial real estate (retail, industrial, mixed-use)

- Some land

The more sellable the property, the more financing options are available. Properties in poor condition or of unusual type that conventional lenders reject are precisely the deals hard money lenders are built to finance.

Hard Money Loan Rates and Costs

Interest Rates

Hard money loan rates currently range from 9%–15% depending on the lender, deal profile, borrower experience, and market conditions, according to sources including LendingTree's 2025 hard money loan overview. The American Association of Private Lenders cites a broader range of 7%–15%.

For context, Freddie Mac's Primary Mortgage Market Survey reported the 30-year fixed-rate mortgage at 6.47% as of mid-2025. That puts hard money rates roughly 3–9 percentage points above conventional financing — a spread borrowers pay for speed, flexibility, and access.

Points and Fees

Beyond the interest rate, budget for:

- Origination points: Typically 1–5 points (1 point = 1% of the loan amount), paid at closing

- Appraisal or BPO fees

- Closing costs

- Draw inspection fees — charged each time rehab funds are released

- Extension fees — if the project runs past the original loan term

- Prepayment penalties — on some loan structures

The total cost of borrowing — not just the interest rate — determines whether the deal's ROI pencils out. A loan at 10% with 4 points and multiple inspection fees may cost more than a 12% loan with 1 point and no draw fees.

Loan Structure Summary

| Feature | Hard Money Loan |

|---|---|

| Payment structure | Interest-only monthly payments |

| Principal repayment | Balloon payment at maturity |

| Loan term | 6–24 months |

| Rate type | Fixed (typically) |

If your exit timeline is clear — say, a 9-month flip — a 12-month loan with extension options may suit you well. An uncertain timeline is where the short term becomes a liability, creating real pressure and default risk.

Pros and Cons of Hard Money Loans

Pros

- Speed: Hard money loans can close in days rather than weeks. The Mortgage Bankers Association's Q1 2025 data shows conventional broker wholesale channel loans averaging 33.8 days from application to closing — a timeline that kills competitive deals.

- Flexibility: Borrowers with complex financial profiles, recent credit events, or non-conforming properties can still access capital. Distressed properties, commercial assets outside bank standards, and income-documentation challenges are all workable here.

- Asset-based underwriting: The property secures the loan, shifting the focus away from the borrower's personal financial history toward the deal's economics.

Cons

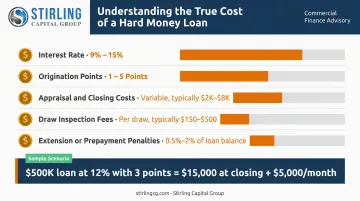

Higher cost: The combination of higher interest rates, origination points, and multiple fees makes hard money significantly more expensive than conventional financing. On a $500,000 loan at 12% with 3 points, you're paying $15,000 at closing plus $5,000 per month in interest — before any draw fees or extensions.

Compressed timeline: Short loan terms create real pressure. Project delays, unexpected renovation costs, or a slow sales market can quickly erode returns or push a borrower toward default — and in states with nonjudicial foreclosure laws, lenders can move fast.

Not the right tool for every deal: Hard money is a poor fit when margins are thin, ARV is speculative, or there's no clear exit strategy. If the deal qualifies for conventional financing, forcing it through a hard money structure wastes money.

How to Find and Evaluate the Right Hard Money Lender

Where Hard Money Lenders Come From

Banks and credit unions don't offer these loans. Sources include private investment companies, specialty real estate lenders, private equity groups, and commercial finance consultants. Quality, terms, and experience across these lenders vary enormously.

Key Questions to Ask Every Lender

Before committing, get answers to:

- What is your maximum LTV and ARV cap?

- What are your standard loan terms and extension options?

- Do you offer interest-only payment structures?

- What are all fees — origination, closing, draw inspections, prepayment penalties?

- What documentation do you require?

- What is your typical time to close?

- Do you have experience with my specific property type and deal structure?

Watch for lenders who are vague on fees, can't demonstrate experience with your property type, or push standard terms without evaluating your specific deal.

Working with a Commercial Finance Consultant

Evaluating dozens of lenders independently takes time that competitive deals don't allow. Working with a consultancy like Stirling Capital Group — which maintains relationships with over 60 private lending sources and is authorized to pre-qualify and pre-underwrite on their behalf — addresses that constraint.

What that authorization means in practice: before a file reaches any lender, Stirling's team evaluates the property, collateral, LTV/ARV ratios, exit strategy, and deal structure. The transaction arrives pre-vetted and aligned to that lender's specific credit criteria, compressing the approval timeline and reducing back-and-forth significantly.

Beyond speed, this model surfaces options a single lender can't offer. Stirling's network covers both debt and equity capital solutions, which matters when a hard money loan covers only part of the capital stack and the remaining gap needs to be filled through preferred equity or a joint venture structure.

For real estate investors specifically, Stirling supports:

- Fix-and-flip acquisitions and distressed property purchases

- Time-sensitive closings and auction deals

- Interest-only payment structures and renovation draw schedules

- High-leverage financing based on LTC, LTV, or ARV

A free consultation is a practical first step. Stirling's team conducts a thorough business analysis before recommending a lending approach — no obligation, no commitment. Reach them at 614-470-4716, info@stirlingcg.com, or through the contact form at stirlingcg.com.

Frequently Asked Questions

How does a hard money lender work?

Hard money lenders are private companies or investors that fund short-term loans secured by real estate, basing approval on the property's value and deal strength rather than the borrower's credit or income. Once approved, funds can be available in days — a speed that conventional lenders can't match.

How risky is a hard money loan?

The primary risks are high costs, compressed timelines, and foreclosure exposure if you default. High rates and fees raise your carrying costs, while short terms create real pressure to sell or refinance on schedule. Going in without a clear exit strategy and adequate cash reserves is how deals go sideways.

How much down do you need for a hard money loan?

Most hard money lenders require 20%–40% down, or equivalent equity. The exact amount depends on the lender, the deal's LTV or ARV ratio, and the borrower's track record — with more experienced investors and stronger deals sometimes accessing higher leverage.

What credit score do you need for a hard money loan?

Many hard money lenders have no formal minimum because approval is based primarily on the property's value. Some lenders do set minimums in the 600–650 range. A stronger credit profile can help secure better rates and terms, but it's rarely the deciding factor.

What is the typical interest rate on a hard money loan?

Current market rates typically range from 9%–15%, though the American Association of Private Lenders cites a broader range starting at 7%. Each private lender sets rates individually based on the deal, borrower profile, and local market conditions. Either way, expect to pay significantly more than a conventional 30-year mortgage.

What is the difference between a hard money loan and a conventional mortgage?

The core difference is speed, cost, and who qualifies. Hard money loans are short-term (6–24 months), asset-based, and close in days — but carry higher rates. Conventional mortgages offer lower rates and 15–30 year terms, but require strong credit and income verification, with closing timelines averaging 34–39 days.