Introduction

You've found a compelling investment property — the price is right, the timing is right, but your capital is tied up in existing equity. Now you need to move fast and choose the right financing tool. Pick wrong, and you could miss the deal entirely or lock yourself into repayment terms that don't fit your exit strategy.

Bridge loans and HELOCs both pull from equity to solve this problem. But they solve it in different ways, with distinct risk profiles, timelines, and qualification requirements. Treating them as interchangeable is one of the most expensive mistakes real estate investors make.

This guide breaks down how each tool works, where each excels, and which situations clearly favor one over the other.

Key Takeaways

- Bridge loans deliver a lump sum quickly — purpose-built for urgent, time-sensitive closings

- HELOCs offer revolving access to capital over time, but require advance setup before a deal is live

- Underwriting differs too — bridge loans are asset-based, while HELOCs rely on income and credit scores

- A HELOC attaches a lien to your primary residence — a meaningfully different risk than a bridge loan secured by the investment property

- The right choice depends on your timeline, deal size, and how clearly your exit strategy is defined

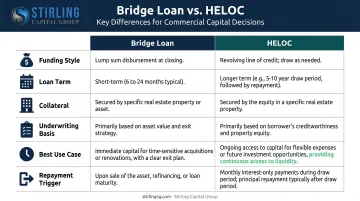

Bridge Loan vs. HELOC: At-a-Glance Comparison

| Feature | Bridge Loan | HELOC |

|---|---|---|

| Funding Style | Lump sum | Revolving credit line |

| Loan Term | 12–36 months | Draw period up to 10 years; repayment up to 20 years |

| Interest Rate Type | Floating (tied to SOFR or similar index) | Variable (tied to U.S. Prime Rate + margin) |

| Collateral | Investment or commercial property | Primary residence |

| Credit Requirements | Sponsor strength, LTV, exit strategy | FICO 660+ with income documentation |

| Best Use Case | Time-sensitive acquisition or transitional asset | Flexible, ongoing capital access |

| Repayment Trigger | Property sale or permanent refinance | End of draw period |

Both products are equity-backed, but that's where the similarity ends. Bridge loans are transactional instruments built around a specific deal and a defined exit — property sale or refinance. HELOCs are long-duration credit facilities underwritten against your home equity and personal financials. Choosing between them depends less on which looks cheaper and more on which structure actually matches your timeline, collateral, and capital purpose.

What Is a Bridge Loan?

A bridge loan is short-term financing designed to close the gap between an immediate capital need — property acquisition, renovation funding, or a down payment — and a future liquidity event such as a sale or permanent refinance. Per the OCC's Commercial Real Estate Lending handbook, bridge loans allow newly acquired or constructed commercial properties to reach stabilization before transitioning to permanent financing.

How Bridge Loans Are Structured

Most bridge loans are interest-only, floating-rate instruments. Lenders like Lument set standard terms of 12–36 months, while Greystone references up to three years including extensions. Rate structures are typically tied to 1-Month CME Term SOFR plus a market spread — not a fixed rate.

On LTV, institutional CRE lenders such as Greystone allow up to 80% of current value, with CBRE's LIHTC bridge program reaching 85% LTV in certain scenarios.

Asset-Based Underwriting: The Key Differentiator

The defining characteristic of bridge loans — especially for investors — is asset-based underwriting. Lenders evaluate:

- Property value and LTV ratio

- Debt Service Coverage Ratio (DSCR)

- Sponsor experience, net worth, and liquidity

- Viability of the exit strategy (sale or refinance)

This matters because investors with strong collateral but inconsistent income documentation often don't fit conventional bank credit boxes. Bridge loans don't require the same debt-to-income analysis that disqualifies many asset-heavy borrowers from bank financing.

Advantages and Trade-Offs

Fast closings, interest-only payments, and flexibility in competitive markets make bridge loans a practical tool for investors who can't wait on conventional timelines:

- JPMorgan reports closing commercial bridge loans in under 30 days

- Interest-only payments preserve cash flow during the hold period

- No requirement to sell before buying

- Avoids sale-contingent offers in competitive markets

The trade-offs are real, though:

- Higher rates than conventional financing

- Short repayment window creates pressure if the exit slips

- Commitment fees, exit fees, and legal costs add to total carry

Traditional banks often have rigid credit requirements for bridge loans, particularly on commercial and investment real estate. When a transaction falls outside standard underwriting guidelines — or when timing is the issue — investors need lenders who can move quickly.

Stirling Capital Group's network of over 60 private lending sources, including bridge lenders, debt funds, private credit funds, and specialty finance providers, gives investors access to bridge capital in those situations. The firm holds authorization to pre-qualify, pre-underwrite, and originate, which cuts the timeline for time-sensitive acquisitions.

Common Bridge Loan Use Cases

- Acquiring a multifamily property before existing equity is liquidated

- Funding a fix-and-flip while awaiting sale proceeds on another asset

- Covering a down payment on commercial property when permanent financing isn't yet secured

- Bridging from construction completion to a long-term refinance or sale

Scenario: An investor identifies a 12-unit multifamily building at a competitive price, but equity is locked in another property that hasn't sold yet. A bridge loan closes the acquisition in under 30 days. Three months later, the existing property sells, the bridge loan is repaid, and the investor transitions to permanent agency financing.

What Is a HELOC?

A HELOC (Home Equity Line of Credit) is a revolving credit line secured against the equity in a borrower's existing property — typically their primary residence. It functions like a credit card backed by real estate: draw funds up to your approved limit, repay, and redraw during the draw period.

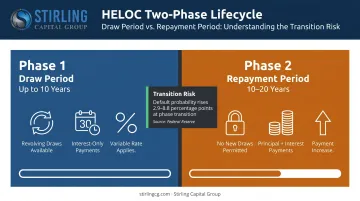

The Two-Phase Structure

Understanding the phase transition is critical, particularly for investors using a HELOC as acquisition capital:

- Draw period — Typically up to 10 years, per the CFPB. Interest-only payments apply on amounts withdrawn.

- Repayment period — Often 10–20 years. No new draws permitted; principal + interest payments begin.

That payment jump at the end of the draw period carries real risk. Federal Reserve research (FEDS 2015-073) found the transition to repayment raises default probability by 2.9 percentage points on average — rising to 8.8 percentage points for higher-risk borrowers (FICO below 725, CLTV above 80%).

Qualification Requirements

HELOCs are income- and credit-driven. Lenders typically require:

- FICO score of 660+ (U.S. Bank, Bank of America both confirm this threshold)

- At least 15–20% equity in the home

- Verified income documentation (pay stubs, W-2s, tax returns)

- Favorable debt-to-income ratio

That's a different model than asset-based bridge lending, where property value and exit strategy — not income documentation — drive approval.

The Risk Investors Underestimate

A HELOC attaches a lien to your primary residence. If an investment deal underperforms or a payment is missed, the family home is at risk. That's a different risk profile entirely from a bridge loan secured by the investment property itself — and one that deserves a hard look before committing home equity to a speculative deal.

Common HELOC Use Cases

HELOCs work best when:

- The credit line is opened before a deal is under contract

- Capital needs are variable or incremental (renovations, carrying costs)

- The borrower wants a pre-approved reserve available for future opportunities

- Rate sensitivity is a priority over speed

TD Bank notes that a home equity line final decision can take 30–45 days. When a purchase deadline is already close, a HELOC won't move fast enough.

Which Option Is Right for You?

Neither is universally better. Four factors should drive the decision.

1. Timing and Urgency

If a deal is already under contract or a competing offer is in play, a bridge loan wins on speed. Bridge lenders are designed for urgent closings. HELOCs require advance underwriting — they're a planning tool, not a reactive one.

2. Transaction Size and Capital Access

HELOCs are capped by your home equity. If the investment property is worth significantly more than the available home equity, a bridge loan can provide more capital — up to 80% LTV on the commercial or investment asset itself. On a $3M acquisition, that difference in accessible capital can determine whether you can close at all.

3. Risk Tolerance

A HELOC is more flexible during the draw period and typically carries lower rates — but it pledges your home as collateral. A bridge loan is more rigid (lump sum, defined payoff trigger) but confines the risk to the investment asset. Keeping your primary residence out of the collateral equation is often reason enough to choose bridge financing.

4. Repayment Certainty

Bridge loans require a clear exit strategy. If you have a pending sale, a refinance commitment, or a defined payoff timeline, a bridge loan is well suited to that scenario. If your capital needs are ongoing and variable — or if the payoff timeline is uncertain — a HELOC's revolving structure is more forgiving.

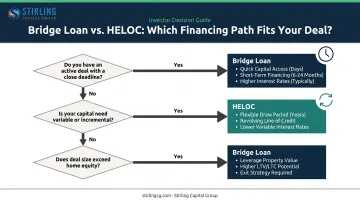

Situational Decision Guide

Choose a bridge loan if:

- You need a lump sum by a specific closing date

- You have a defined exit strategy (pending sale or refinance commitment)

- The transaction size exceeds available home equity

- You want primary residence equity untouched

Choose a HELOC if:

- You've opened the line proactively, before a deal materializes

- Capital needs are variable or spread across multiple uses

- Lower rate cost is a priority over closing speed

- You have the income documentation and credit profile to qualify

Two scenarios, two tools: Investor A opens a HELOC three months before she starts shopping for rental properties. When she finds a duplex, she draws from the line to cover the down payment at a competitive rate — no urgency, no problem. Investor B discovers a commercial acquisition opportunity with a competing offer arriving in 48 hours. He uses a bridge loan to close in under two weeks. The right tool depends entirely on your timeline, your risk profile, and how the deal is structured.

Conclusion

Bridge loans and HELOCs serve different purposes, and the right choice depends entirely on your situation. A bridge loan delivers speed, certainty, and asset-based underwriting that works when banks won't. A HELOC offers lower cost and flexibility — but only when timing is not urgent and the credit line is already in place.

At a glance:

- Bridge loan: best for fast closes, investment-scale acquisitions, and asset-based deals

- HELOC: best for flexible, lower-cost access when you can plan ahead

Both tools use equity as collateral and carry real repayment risk. Choosing the wrong structure for your timeline or collateral type can turn a sound investment into a cash flow problem — one that's difficult to unwind once the deal is closed.

Working with an advisor who can evaluate multiple options across multiple lenders is how experienced investors avoid that outcome. Stirling Capital Group's network of over 60 private lending sources includes bridge lenders, debt funds, specialty finance providers, and private credit funds — giving entrepreneurs, investors, and developers access to the right capital structure for the right transaction.

Contact Stirling Capital Group for a free consultation: call 614-470-4716, email Info@StirlingCG.com, or visit www.StirlingCG.com to discuss your transaction and find the financing structure that fits your timeline and deal structure.

Frequently Asked Questions

How much does a bridge loan cost?

Bridge loan costs typically include a floating interest rate (tied to SOFR plus a spread), origination fees in the 0.50%–1.0% range, exit fees around 2%, and legal or third-party expenses. Extension fees apply if the payoff timeline stretches. Total carry cost depends on loan size, lender terms, and how long the loan is held.

What is the difference between a home equity loan and a HELOC?

A home equity loan disburses a lump sum at a fixed rate with immediate repayment — structured and predictable. A HELOC is a revolving credit line with a variable rate and a draw period, letting you borrow only what you need. Both use the home as collateral.

Can you use a HELOC to buy an investment property?

Yes. Borrowed funds secured by an asset are an acceptable source for down payment and closing costs. The key caveat: the HELOC payment must be factored into your debt-to-income ratio when underwriting the investment property mortgage, which can reduce your qualifying capacity for the new loan.

What credit score do you need for a bridge loan vs. a HELOC?

HELOC lenders (U.S. Bank, Bank of America) confirm a 660+ FICO requirement. For commercial bridge loans, institutional lenders focus more on sponsor experience, net worth, liquidity, DSCR, and exit strategy than a specific FICO threshold — though asset-based private lenders, including those in Stirling Capital Group's network, apply more flexible underwriting criteria than conventional institutions.

Which is faster to fund — a bridge loan or a HELOC?

Bridge loans are faster for time-sensitive transactions. JPMorgan reports closing commercial bridge loans in under 30 days. TD Bank notes that a HELOC final decision can take 30–45 days — and that's before funds are available to draw. If a deal is already live, a bridge loan is the purpose-built instrument.

What happens if my home doesn't sell before my bridge loan is due?

Lenders may offer extensions on a case-by-case basis, commonly up to six months, with extension fees and higher carrying costs attached. If a sale or refinance still can't close, refinancing the bridge into longer-term financing becomes the next option. A realistic, documented exit strategy should be in place before taking one out.