That's where the DSCR vs. conventional debate gets real. Both loan types are legitimate paths to investment property financing, but they're built on completely different logic. Choosing the wrong one doesn't just cost you a slightly higher rate — it can stall your entire acquisition pipeline.

This guide breaks down how each loan works, compares them head-to-head, and gives you a practical framework for deciding which fits your current situation.

Key Takeaways

- DSCR loans qualify based on a property's rental income — no W-2s, no DTI calculation required

- Conventional loans typically offer lower rates but cap financed properties at 10 total and require full personal income verification

- DSCR loans generally require 20–25%+ down, while conventional investment loans may accept as little as 15% on a single-unit property

- Self-employed investors and growing portfolios are the clearest DSCR use cases

- Many experienced investors use both structures strategically — not one exclusively

DSCR Loans vs. Conventional Loans at a Glance

The table below compares the two loan types across the factors that matter most to real estate investors — from qualification requirements to eligible property types.

| Factor | DSCR Loans | Conventional Investment Loans |

|---|---|---|

| Primary qualification basis | Property rental income / DSCR ratio | Borrower personal income and DTI |

| Income documentation | Not required | W-2s, tax returns, pay stubs |

| DTI ratio evaluated | No | Yes (typically max 36–45%) |

| LLC ownership allowed | Yes, commonly supported | Generally not for standard agency loans |

| Portfolio scalability | No hard cap | Fannie/Freddie cap at 10 financed properties |

| Typical down payment | 20–25%+ (up to 30% in some scenarios) | 15% (1-unit) / 25% (2–4 unit) |

| Interest rate outlook | Higher — typically 150–250 bps above conforming | Lower for qualified borrowers |

| Speed to close | Generally faster — fewer documentation hurdles | Slower — extensive personal file review |

| Eligible property types | SFR, 2–4 unit, STR, small multifamily, mixed-use (varies by lender) | Primarily 1–4 unit residential |

| Ideal investor profile | Self-employed, complex income, growing portfolio | W-2 income, first or second rental, low DTI |

Actual terms vary by lender, property type, borrower credit, and market conditions. Confirm specifics with a qualified lending advisor before making financing decisions.

What Is a DSCR Loan?

DSCR stands for Debt Service Coverage Ratio — and it's the entire premise of how these loans underwrite. Instead of evaluating your income, the lender evaluates the property's income relative to its debt obligations.

The formula: DSCR = Net Operating Income ÷ Total Debt Service

What different ratios signal:

- Below 1.0 — The property doesn't cover its own debt payments

- 1.0 — Break-even; rent exactly covers the loan payment (PITIA)

- 1.25+ — A cash-flow buffer exists above debt obligations; Kiavi notes this is generally considered "good" coverage

Most DSCR lenders require a minimum ratio between 1.0 and 1.25, though some offer "no-ratio" programs for properties below 1.0 with additional conditions and higher credit score requirements.

On the underwriting side, lenders skip tax returns and pay stubs entirely — instead, they analyze rent rolls, lease agreements, and appraisal-based market rent estimates.

Why Investors Use DSCR Loans

For the right investor, the structural advantages are hard to ignore:

- No personal income verification — qualification hinges on the property, not your W-2

- No DTI calculation — your existing debt load doesn't limit approval

- LLC-eligible — most DSCR lenders allow closing through an LLC or corporation, which conventional programs typically don't support

- No hard cap on properties financed — each deal is evaluated independently

The tradeoff: DSCR loans price higher than conventional loans. National Mortgage Professional's 2025 non-QM investor guide cites DSCR coupons pricing 150–250 basis points above conforming rates. The underwriting flexibility shifts more risk to the lender, and that gets priced directly into the rate.

Who DSCR Loans Serve Best

This structure works particularly well for:

- Self-employed borrowers whose write-offs reduce reported income below conventional qualifying thresholds

- Investors with multiple rentals already on their books

- Buyers using BRRRR or fix-to-rent strategies, where projected market rent drives underwriting

- Anyone who needs to close faster or hold property under an LLC for asset protection

What Is a Conventional Investment Property Loan?

Conventional loans are traditional mortgages not backed by the federal government — offered through banks, credit unions, and GSE-backed channels (Fannie Mae and Freddie Mac). These loans qualify you, not the property: credit score, employment history, verified income, and debt-to-income ratio drive the decision.

The Case for Conventional

For investors who qualify comfortably, the advantages are real:

- Prices tighter than DSCR loans, keeping your rate at the lower end of the investment property range

- Allows as little as 15% down on single-unit purchases (Fannie Mae and Freddie Mac permit up to 85% LTV)

- Follows standard documentation and well-understood approval criteria familiar to most lenders

According to Bankrate's current investment property rate data, investment property mortgage rates typically run 1–2% above owner-occupied loans. Conventional keeps you at the lower end of that range; DSCR pushes toward the higher end.

The Structural Limits Investors Run Into

Those rate advantages come with real constraints — ones that tend to surface as your portfolio grows:

- Hits a DTI wall fast — Fannie Mae caps manual underwriting at 36% DTI (45% under specific conditions), and every new rental pushes that number higher

- Stops at 10 financed properties — Fannie Mae and Freddie Mac both limit borrowers to 10 financed 1–4 unit properties, primary residence included

- Requires a full documentation package — W-2s, two years of tax returns, pay stubs, and complete asset verification, which slows deal timelines

When Conventional Makes Sense

- First or second rental property with straightforward W-2 income

- Excellent credit, low personal debt load, and a clean qualifying file

- Long-term hold strategy where the lowest possible rate drives cash flow math

DSCR vs. Conventional: Key Differences Investors Need to Know

Income Verification and DTI

The underwriting divide is fundamental: conventional lenders evaluate the borrower first; DSCR lenders evaluate the property first.

Self-employed investors often show significantly reduced taxable income after legitimate business deductions — which looks damaging on a conventional application but has no bearing on a DSCR evaluation. The property's income does the qualifying, not the borrower's tax return.

Landlords with high depreciation losses face a similar problem: Schedule E may show paper losses even when actual cash flow is strong. Under DSCR underwriting, those paper losses are irrelevant.

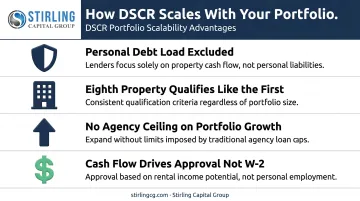

Portfolio Scalability

This is the most consequential difference for active investors. Every conventional loan you take adds to your personal DTI and counts toward the 10-property agency ceiling. When you hit that ceiling — which happens faster than most investors expect — conventional financing simply stops being an option.

DSCR loans work differently. Each property is evaluated independently:

- Your personal debt load doesn't factor into the property's approval

- The eighth property qualifies on the same terms as the first

- No agency ceiling caps your portfolio growth

- Cash flow from the property — not your W-2 — drives the decision

For investors building a portfolio with any real momentum, this structural difference is decisive.

Down Payment and LTV Requirements

A direct comparison:

| Property Type | DSCR Loan (Typical) | Conventional (Agency Max LTV) |

|---|---|---|

| Single-unit investment | 20–25% down | 15% down (85% LTV) |

| 2–4 unit investment | 20–30% down | 25% down (75% LTV) |

DSCR's higher equity requirements reflect the lender's risk-adjusted pricing for offering underwriting flexibility. For single-unit properties, conventional can actually require less upfront capital — though the income qualification requirements offset that advantage for many investors.

Interest Rates and Cash Flow Impact

The rate premium on DSCR loans is real, and investors need to do the math. On a $300,000 loan, a 1.5% rate difference translates to roughly $270–$280 more in monthly debt service — meaningful when you're evaluating cash flow on a property returning $2,200/month in rent. At some portfolio scale and income complexity, that premium is the price of being able to close the deal at all. If you have clean W-2 income and are financing your first rental, qualifying conventionally saves real money — and that's the right move.

Which Loan Is Right for Your Investment Strategy?

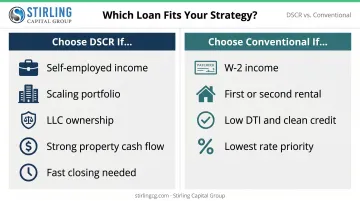

Choose DSCR if:

- Your income is self-employed, irregular, or reduced by write-offs

- You own multiple rentals or plan to scale quickly

- You're investing through an LLC and want liability protection

- The property's cash flow can carry the deal independently

- You need faster, more certain execution on a competitive acquisition

Choose conventional if:

- You have strong, easily documented W-2 income

- You're financing your first or second rental

- Your DTI is low and credit is clean

- You're prioritizing the lowest possible rate for a long-term hold

Many experienced investors don't choose one structure permanently — they use both. Conventional financing for early properties with favorable rate economics, DSCR for expansion once personal income becomes a limiting factor or LLC ownership becomes a priority.

If you're evaluating a specific property or need help choosing the right structure, Stirling Capital Group works with over 60 private lending sources across DSCR, conventional, bridge, and portfolio programs. Instead of forcing your deal into a single lender's credit box, the team compares structures side-by-side to find the right fit. Schedule a free consultation at 614-470-4716 or info@stirlingcg.com.

Conclusion

Neither loan type is universally better. DSCR loans trade higher rates for flexibility, speed, and the ability to scale without hitting personal income ceilings. Conventional loans trade stricter qualification requirements for lower costs — a worthwhile exchange for investors whose financial profiles fit the mold.

The right choice depends on your income documentation, portfolio size, closing timeline, and how well the property's cash flow stands on its own. As your portfolio grows and your financial picture gets more complex, having access to both financing paths — rather than being locked into one lender's options — becomes increasingly valuable.

That's where working with a capital advisor like Stirling Capital Group makes a practical difference. With access to over sixty lending sources across both conventional and private channels, the right financing path becomes a strategic choice — not a constraint.

Frequently Asked Questions

Are DSCR loans better than conventional loans?

Neither is universally better. DSCR loans offer more flexibility and scalability for investors with complex income or growing portfolios, while conventional loans typically deliver lower rates for borrowers with strong documented income. The best choice depends on your financial profile, portfolio stage, and how the specific property cash flows.

Do DSCR loans require 20% down?

Most DSCR lenders require a minimum of 20–25% down, with some scenarios requiring 25–30% depending on property type, deal complexity, and DSCR ratio strength. Conventional investment loans may accept as little as 15% down on single-unit properties but come with stricter income and DTI requirements.

What DSCR ratio do I need to qualify?

Most lenders look for a minimum DSCR of 1.0 to 1.25, with stronger ratios (1.25+) generally unlocking better pricing and terms. Some lenders offer "no-ratio" programs for properties below 1.0, though these carry additional credit score requirements and higher reserve minimums.

Can self-employed investors use DSCR loans?

DSCR loans are well-suited for self-employed borrowers since qualification is based on property rental income, not personal tax returns. Write-offs and Schedule E losses don't factor into the underwriting decision at all.

Can I close a DSCR loan under an LLC?

Most DSCR lenders allow borrowers to close under an LLC or corporation — something conventional loans typically don't accommodate. This makes DSCR loans a stronger fit for investors prioritizing liability protection and clean separation between personal and investment assets.

Can I refinance from a conventional loan into a DSCR loan?

Yes. Once a property is stabilized and generating sufficient rental income, refinancing into a DSCR structure removes personal income requirements from underwriting and frees up conventional loan capacity for future acquisitions. Stirling Capital Group advises investors on this transition across both loan structures.