Introduction

Choosing between the SBA 504 and 7(a) loan programs sounds simple until you're actually in the decision. Both carry the SBA's backing and offer longer repayment terms than conventional bank loans — yet they're built for fundamentally different purposes.

Pick the wrong one and you could be locked into the wrong rate structure, facing unexpected collateral demands, or simply ineligible for the funds you need.

In FY2025, the SBA approved 77,600 loans totaling $37 billion through the 7(a) program, and 6,750 loans totaling $7.8 billion through the 504 program — tens of thousands of businesses that faced this exact choice.

This guide breaks down how each program works, where they diverge, and how to determine which one matches your specific capital need.

Key Takeaways

- The SBA 504 targets fixed assets — commercial real estate, construction, heavy equipment — with fixed rates and a minimum 10% down payment.

- The SBA 7(a) is the SBA's most flexible program, covering working capital, business acquisitions, inventory, and real estate (typically at variable rates).

- 504 loans involve three parties (borrower, bank, CDC); 7(a) loans run through a single bank lender.

- Both loans can be used together in a "piggyback" structure for complex acquisitions with mixed capital needs.

- Choosing between them comes down to your use of funds, your hold period, and how much rate certainty matters to your deal.

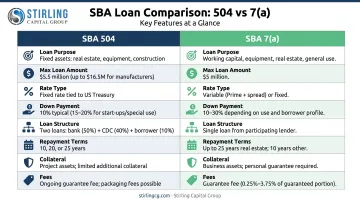

SBA 504 vs. 7(a): Quick Comparison

| Feature | SBA 504 | SBA 7(a) |

|---|---|---|

| Loan Purpose | Fixed assets only (real estate, equipment) | Broad: working capital, acquisitions, inventory, real estate, debt refinancing |

| Maximum Loan Amount | $5.5M (higher for manufacturers/energy projects) | $5M |

| Interest Rate Type | Fixed (tied to 10-year Treasury at funding) | Variable (Prime + spread); fixed options rare |

| Current Rate Range | ~5.9%–6.2% effective (as of June 2026) | ~9.75%–13.25% variable maximum |

| Down Payment | 10% standard; 15–20% for startups or special-purpose buildings | No universal requirement; lender-determined |

| Loan Structure | Three-party: bank (50%), CDC (40%), borrower (10%) | Single lender |

| Repayment Terms | 10, 20, or 25 years | Up to 10 yrs (working capital/equipment); up to 25 yrs (real estate) |

| Collateral | Project assets; no "All Collateral Available Test" | All available business assets; personal real estate may be required |

| Upfront Guarantee Fee (FY2026) | 0.50% | 0%–3% based on loan size |

| Annual Service Fee (FY2026) | 0.209% | 0.55% of guaranteed portion |

On interest rates: The 504's fixed rate is locked at funding based on the 10-year Treasury (currently 4.49% as of June 2026) plus a spread. The 7(a) variable rate tracks the Prime Rate (currently 6.75%) plus a lender spread — up to 3% for loans over $350,000, and up to 6.5% for loans under $50,000. According to NerdWallet, roughly 80% of 7(a) loans carry variable rates.

What Is the SBA 504 Loan?

The SBA 504 loan was built as an economic development tool — its explicit purpose is to help small businesses acquire and improve long-term, fixed assets without requiring substantial upfront capital. Unlike general-purpose financing, it's designed specifically for business owners making long-term fixed-asset investments.

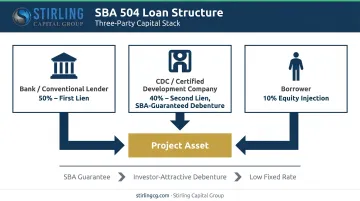

The Three-Party Structure

This is where the 504 differs most visibly from any other SBA product. The loan involves three separate parties:

- Bank (conventional lender): Finances 50% of the project, holds first lien

- CDC (Certified Development Company): Provides 40% via an SBA-guaranteed debenture, holds second lien

- Borrower: Contributes a minimum 10% equity injection

CDCs are non-profit corporations certified and regulated by the SBA specifically to package, process, close, and service 504 loans. Their involvement is what enables the favorable down payment and fixed-rate structure: the SBA's guarantee makes the CDC debenture attractive to investors, which keeps the rate low.

Down payment requirements scale upward in specific circumstances:

- 15% for startup businesses or special-purpose buildings

- 20% if the business is both a startup and uses a special-purpose building

The Fixed Rate Advantage

The 504's fixed rate is locked at the time the debenture is sold — tied to the 10-year U.S. Treasury rate plus a spread covering CDC fees and SBA servicing costs. Current effective rates from CDC Small Business Finance show 5.876% for 10-year, 6.164% for 20-year, and 6.112% for 25-year terms (as of June 11, 2026). That rate doesn't move. Ever. For a 25-year loan in a rising rate environment, that certainty compounds into significant savings.

What the 504 Cannot Do

The 504 is strictly off-limits for:

- Working capital or operating expenses

- Inventory purchases

- Speculative or investment real estate

- Intellectual property or consulting fees

If any portion of your capital need falls into these categories, the 504 alone won't cover it.

Use Cases for the SBA 504

The strongest applications include:

- Purchasing an owner-occupied commercial building

- Constructing a new facility from the ground up

- Acquiring major manufacturing or production equipment

- Refinancing existing debt tied to qualifying fixed assets

Manufacturers and energy-saving projects often qualify for a higher SBA debenture cap — up to $5.5M — making this program particularly attractive for those sectors. In FY2026, the SBA also waived both the upfront guaranty fee and annual service fee entirely for small manufacturers (NAICS codes 31–33).

What Is the SBA 7(a) Loan?

The 7(a) is the SBA's flagship program — and its most used. In FY2025, it accounted for more than 11 times the number of approvals as the 504, reflecting its broader eligibility and wider range of uses. That reach comes from one thing: flexibility. The 7(a) covers more use cases than any other SBA program.

Eligible Uses

The 7(a) covers nearly every phase of a business's lifecycle:

- Working capital (short- and long-term)

- Inventory purchases and supplies

- Equipment, machinery, furniture, and fixtures

- Owner-occupied commercial real estate

- Leasehold improvements

- Business acquisitions (including goodwill)

- Debt refinancing

This breadth is the 7(a)'s defining advantage. A borrower can fund a business purchase — including the intangible value of the brand — with a single 7(a) loan. The 504 cannot touch goodwill.

Variable Rate Structure and Rate Risk

Most 7(a) loans price at the Prime Rate plus a lender spread. With Prime currently at 6.75%, a loan over $350,000 carries a maximum rate of 9.75% — and loans under $50,000 can reach 13.25%. Fixed-rate 7(a) options exist but are uncommon and typically only available on shorter terms.

That variability matters over a 25-year term. A rate that starts at 9.75% and rises over the life of the loan looks very different on a payment schedule than a fixed 6.1% 504 rate.

The "All Collateral Available" Test

Rate exposure is only part of the picture. Collateral requirements introduce a separate layer of personal financial risk. For 7(a) loans, if a lender identifies a collateral shortfall, they may be required to take a lien against the borrower's personal real estate — provided the equity in that property exceeds 25% of its fair market value. That lien can encumber a borrower's home — a direct personal liability that 504 loans avoid, since the project assets serve as the primary collateral.

Repayment Terms and Prepayment

- Working capital, equipment, inventory: Up to 10 years

- Commercial real estate: Up to 25 years

- Prepayment penalties: Apply only on loans with maturities of 15 years or longer, and only if the borrower prepays 25% or more of the outstanding balance in the first three years: 5% in year 1, 3% in year 2, 1% in year 3

Use Cases for the SBA 7(a)

The 7(a) is the right tool when:

- You're acquiring an existing business, including goodwill — the 504 cannot finance intangible value

- Mixed-use capital is needed at launch (startup scenarios with multiple funding needs)

- Working capital is the primary need during a growth phase or seasonal cycle

- You're consolidating or refinancing multiple business debt obligations

- Speed matters — single-lender structure closes faster than the 504's three-party coordination

SBA 504 vs. 7(a): Which Loan Is Right for You?

Neither loan is universally better. The right choice comes down to four questions: What is the money for? How long will you hold the asset? How important is rate certainty? And how much personal collateral exposure can you tolerate?

Decision Framework

Choose the SBA 504 if:

- You're buying or building owner-occupied commercial real estate

- You want a fixed interest rate locked in for 10, 20, or 25 years

- You plan to stay in the property long-term

- You want to limit personal collateral exposure beyond the project assets

- Your project exceeds $1 million (where 504 fee structures are often more favorable)

Choose the SBA 7(a) if:

- You need working capital alongside real estate or equipment

- You're acquiring a business, including its goodwill

- Speed of approval is critical (competitive acquisition, tight closing window)

- Your project mixes asset types that don't fit the 504's narrow eligible use list

- You prefer a single lender relationship

The Fee Comparison at Scale

For smaller loans, the fee difference is modest. But as project size increases, the math shifts. FY2026 7(a) upfront guarantee fees graduate with loan size — 1% for loans over $150K to $700K, rising to 3% for loans over $700K to $5M. The 504's upfront guaranty fee stays flat at 0.50% regardless of loan size. On a $3M project, that's a meaningful difference in closing costs.

The Long-Term Rate Calculation

On a 25-year term, a fixed 6.1% 504 loan versus a variable 7(a) starting at 9.75% creates a substantial total interest differential. That gap matters most for borrowers who intend to hold the asset through the full term. If your business plans to sell or relocate within a few years, the calculus changes — the 7(a)'s shorter prepayment penalty window (only years 1–3, only on 15+ year terms) provides more exit flexibility than a 25-year 504 commitment.

When the scenario doesn't fit neatly into either program — a business acquisition blending real estate with working capital, for instance — the right structure may involve SBA financing, private lending, or a coordinated combination of both. At Stirling Capital Group, we help borrowers work through that analysis: eligibility screening, lender matching, and deal structuring across more than 60 commercial lending sources, with no obligation to start.

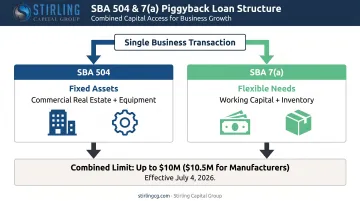

Can You Use Both SBA 504 and 7(a) Loans Together?

Yes. For the right transaction, combining both programs gives borrowers access to more capital across a wider range of uses than either loan can cover alone.

How the Piggyback Structure Works

The strategy pairs each program with the portion of the project it's designed for:

- SBA 504 covers the fixed asset component (commercial real estate, major equipment)

- SBA 7(a) covers the working capital, inventory, or other flexible-use needs

A practical example: a business buyer needs to purchase the property from which they'll operate (504) while also funding opening inventory and working capital (7(a)). Rather than forcing everything into a single loan type — where one or both programs would be stretching beyond their eligible uses — the piggyback structure keeps each loan within its eligible use, which matters when exposure limits are as large as they've become.

Updated Exposure Limits (Effective July 4, 2026)

The SBA recently doubled the cumulative combined limit. Effective July 4, 2026, qualified borrowers can access up to $5M through 7(a) and up to $5M through 504 — a combined $10M. Small manufacturers can combine up to $5M in 7(a) with up to $5.5M in 504, for a combined $10.5M.

Key rules to observe:

- Each loan must independently meet its own program's eligibility requirements

- The two programs must remain structurally separate

- Using 7(a) funds alone for both components is not eligible under this structure

Conclusion

The SBA 504 wins on rate certainty and total cost for long-term fixed asset ownership. The SBA 7(a) wins on flexibility, speed, and breadth of eligible use. Neither is better in the abstract — the right answer depends entirely on what you're buying, how long you're keeping it, and what else your business needs in the same transaction.

For a straightforward real estate purchase with a long hold period, the fixed 504 rate will almost always produce better outcomes than a variable 7(a) over 25 years. For a business acquisition — especially one involving goodwill, inventory, and mixed working capital needs — the 7(a)'s single-lender flexibility often wins.

If your situation involves both, a piggyback structure may be worth a serious look — and that's exactly where having the right advisory perspective matters.

Stirling Capital Group offers a free consultation and business analysis for owners working through this decision. Our team can evaluate your capital needs, screen for eligibility across SBA programs, and determine whether private lending alternatives — or a combination approach — better match your timeline and borrower profile. Reach us at 614-470-4716 or info@stirlingcg.com.

Frequently Asked Questions

What is the main difference between an SBA 504 and 7(a) loan?

The 504 is restricted to fixed assets — owner-occupied real estate, construction, and long-term equipment — with a fixed interest rate and a three-party loan structure. The 7(a) is the SBA's broadest program, covering working capital, business acquisitions, inventory, and real estate through a single bank lender, typically at a variable rate.

Is an SBA 7(a) loan a good idea?

For businesses needing flexible, multipurpose funding — especially acquisitions, working capital, or mixed-use projects — the 7(a) is a strong option. The trade-offs are variable rate risk in rising environments and potential personal real estate collateral requirements if a business asset shortfall exists.

Is it beneficial to separate your business loan into a 7(a) and 504?

The combination can be highly effective when a transaction involves both fixed assets and working capital needs. It allows borrowers to capture the 504's fixed rate advantage for real estate while using the 7(a)'s flexibility for operating needs — provided each loan meets its own program requirements independently.

Can you use an SBA 504 loan for working capital?

No. The SBA 504 loan cannot be used for working capital, inventory, operating expenses, or intellectual property. The 504 strictly limits eligible uses to fixed assets: commercial real estate, construction, and long-term equipment purchases.

How long does it take to get approved for an SBA 504 vs. 7(a) loan?

Standard 7(a) loans typically take one to three months from application to funding. Clean 504 transactions reach initial closing around 60 days, with the debenture takeout occurring 60–90 days after escrow close. Both programs require similar planning horizons, though the 7(a)'s single-lender structure can compress timelines when speed is critical.

What credit score is needed for an SBA 504 or 7(a) loan?

The SBA does not publish a universal minimum credit score for either program. Most SBA-preferred lenders look for a personal credit score of 650 or higher as a starting benchmark, though individual lender requirements vary and other factors — cash flow, collateral, business history, and industry type — carry significant weight alongside the score.