Introduction

Raw materials arrive before revenue does. Workers get paid before customers settle invoices. In manufacturing, cash flows out the door weeks or months before it flows back in — and that gap has consequences.

Working capital gets treated as a balance sheet metric in most finance conversations. For manufacturers, it's something more immediate: it determines whether the factory floor runs tomorrow. A healthy working capital position keeps production moving; a shortfall stops it, regardless of how strong demand might be.

This article breaks down the reasons manufacturing companies need working capital — and what's at stake when it runs thin.

Key Takeaways

- Working capital covers the gap between paying for inputs and collecting from customers — and that gap grows with the business

- Three pressures drive the need: daily production costs, inventory funding, and the receivables-to-payables timing gap

- Cash shortfalls trigger operational breakdowns before financial distress ever shows on a balance sheet

- Manufacturers with strong assets but cash flow constraints have access to financing options beyond traditional bank loans

What Is Working Capital in Manufacturing?

Working capital is current assets minus current liabilities. For most businesses, that's a straightforward calculation. For manufacturers, it's more layered:

Working Capital = Raw Materials + Work in Progress + Finished Goods + Accounts Receivable − Accounts Payable

Each of those asset categories represents cash that's been spent but not yet recovered. Raw materials in the warehouse, products on the production floor, finished goods awaiting shipment, outstanding invoices — every stage ties up cash before a dollar comes back in.

Manufacturing is more working capital-intensive than most industries for three structural reasons:

- Long production cycles — goods take time to produce, extending the period between cash outflow and revenue recognition

- Multi-stage inventory — capital is tied up simultaneously in raw materials, WIP, and finished goods

- Payment timing mismatches — customers often pay in 30–90 days, while suppliers typically expect payment in 15–30 days

The result is a structural cash flow gap built into every production cycle. Working capital is what keeps operations running across that gap — covering payroll, materials, and overhead before customer payments arrive.

Why Manufacturers Need Working Capital: Three Core Reasons

The reasons below reflect real operational conditions manufacturers face, not abstract finance theory. Each one has measurable consequences.

Reason 1: Sustaining Uninterrupted Daily Production

Manufacturing is a continuous-cost environment. Before a single product is sold, the company has already paid for materials, labor, utilities, equipment operation, and overhead. None of those costs wait for customer payments to arrive.

They require liquid capital — cash on hand, not receivables.

When working capital runs short, the consequences hit the factory floor directly:

- Suppliers stop delivering materials when invoices go unpaid

- Equipment maintenance gets deferred, increasing breakdown risk

- Overtime cannot be funded during demand spikes

- Order fulfillment slows or stops even when customer demand is strong

The 2026 Federal Reserve Small Business Credit Survey found that 56% of employer firms seeking financing did so specifically to meet operating expenses. For manufacturers, that figure reflects a persistent reality: production costs don't pause while revenue catches up.

For rapidly expanding manufacturers, the cash burn rate accelerates faster than revenue recognition. More orders mean more upfront costs — materials, labor, production runs — before any of it converts to income. Companies without sufficient working capital face a counterintuitive trap: strong demand they cannot fulfill because they lack the liquidity to fund production.

KPIs affected: Production uptime, order fulfillment rate, days cash on hand, operating cost coverage ratio

When it's most acute: High-growth periods, seasonal demand peaks, after major contract wins, and when entering new markets — all situations where cash outflows precede inflows by weeks or months.

Reason 2: Managing Inventory and Supply Chain Costs

Inventory is the single largest consumer of working capital in manufacturing. A manufacturer must simultaneously fund raw material purchases, active production, and finished goods storage — often for weeks or months — before any of it generates revenue.

Insufficient working capital forces a difficult choice: buy too little inventory and risk production stoppages, or hold too much and tie up cash in stock that depreciates or becomes obsolete. Neither outcome is good.

Supply chain disruptions make this harder to manage. According to the NAM's Q1 2025 Manufacturers' Outlook Survey, 76.2% of manufacturers identified trade uncertainties as a primary business challenge. When tariffs shift or commodity prices spike, manufacturers need room to adjust procurement quickly — which requires available working capital.

Carrying costs compound the problem. APQC benchmarking data puts median inventory carrying cost at 10% of average inventory value annually across industries, encompassing storage, insurance, shrinkage, and obsolescence. For manufacturers running lean margins, that's a meaningful drag on cash.

Supply chain uncertainty can force middle-market manufacturers to carry 60–90 days of additional safety stock, driving working capital requirements up by millions — a buffer that requires liquidity to maintain.

KPIs affected: Inventory turnover rate, days inventory outstanding (DIO), carrying cost as a percentage of inventory value, stock-out frequency

When it's most acute: During commodity price volatility, new tariff cycles, rapid demand shifts, or supply chain disruptions that require fast procurement adjustments without a cash buffer.

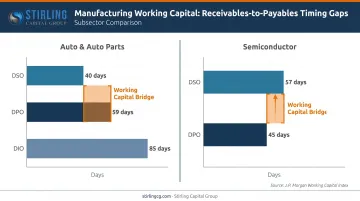

Reason 3: Bridging the Receivables-to-Payables Gap

This is the structural timing problem at the heart of manufacturing finance. Manufacturers routinely extend 30–90 day payment terms to customers — particularly large OEM buyers and wholesale purchasers — while supplier payment terms run much shorter, often 15–30 days. The gap between those two deadlines must be funded by working capital.

J.P. Morgan's Working Capital Index shows this gap clearly across manufacturing subsectors. Auto and auto parts companies carried a DSO of 40 days against a DPO of 59 days and DIO of 85 days. Semiconductor manufacturers showed a DSO of 57 days against a DPO of only 45 days — meaning they were collecting slower than they were paying. In both cases, working capital bridges the difference.

As a manufacturer wins more customers, open receivables grow in proportion. More sales mean more capital locked in unpaid invoices at any given time. Without working capital to cover the gap, the next production cycle cannot start — regardless of how promising the order book looks.

Meanwhile, operating costs don't pause. Payroll runs, rent is due, utilities keep billing, and supplier invoices arrive — all on their own timelines, indifferent to when customers choose to pay.

There's a downstream risk worth noting: chronic late payments to suppliers erode negotiating leverage over time. Suppliers may tighten payment terms, reduce credit limits, or deprioritize your orders. The receivables gap doesn't stay a finance problem — it becomes a supply chain problem.

KPIs affected: Days sales outstanding (DSO), days payable outstanding (DPO), cash conversion cycle (CCC), accounts receivable aging

When it's most damaging: During rapid scaling (more open invoices simultaneously), when a major customer delays payment, or when supplier deadlines tighten due to market conditions.

What Happens When Working Capital Runs Short

The warning signs appear on the factory floor before they appear on a financial statement. The operational cascade typically unfolds in this order:

- Raw material orders get delayed or reduced

- Production slows to match available inputs

- Delivery timelines slip, affecting customer commitments

- Customer relationships deteriorate as reliability declines

Each disruption in that chain triggers a financial ripple. The downstream consequences compound quickly:

- Unfulfillable orders — confirmed demand becomes a liability when there's no capital to produce against it

- Expensive emergency borrowing — credit cards and high-cost short-term instruments fill gaps at significant cost

- Supplier relationship damage — chronic late payments lead to worse terms or supply cutoffs

- Missed investment windows — equipment upgrades, market entry, or technology adoption that competitors can fund

- Insolvency risk — SCORE reports that cash flow failure — not unprofitability — is the primary reason small businesses close their doors

A manufacturer can be profitable on paper and still fail operationally. When working capital can't bridge the gap between production and payment, even a healthy order book offers no protection.

How Manufacturers Can Access the Working Capital They Need

Traditional bank financing often doesn't fit manufacturing timelines. Approval processes are lengthy, documentation requirements are extensive, and credit decisions frequently rely on trailing earnings rather than the strength of a manufacturer's assets or order book.

Manufacturers have several alternatives:

| Financing Type | Best For |

|---|---|

| Revolving lines of credit | Ongoing operating expense coverage with recurring draw-and-repay |

| Invoice factoring / AR financing | Accelerating cash from outstanding invoices |

| Asset-based lending (ABL) | Borrowing against receivables, inventory, and equipment |

| Purchase order financing | Funding confirmed customer orders before production |

| Trade finance facilities | Bridging the full cycle from supplier payment to customer collection |

For manufacturers declined by conventional banks — or those who need capital faster than institutional timelines allow — Stirling Capital Group offers a consultative alternative. Instead of applying a one-size-fits-all underwriting model, the firm evaluates the complete supply chain cycle and matches each situation with the most appropriate lender from a network of 60+ private and specialty financing sources.

That network spans bank ABL groups, non-bank lenders, private credit funds, and specialty finance providers — many of which specifically understand inventory valuation, receivables dynamics, and purchase order economics.

To help manufacturers identify the right structure before committing to an application, Stirling Capital Group provides a free consultation and business analysis tailored to each company's operational profile.

Conclusion

Working capital is what keeps manufacturing in motion. Without it, raw materials don't arrive, production stalls, workers go unpaid, and customer orders get missed, even when demand is strong and the business is otherwise healthy.

The three pressures covered here — sustaining daily production, managing inventory costs, and bridging the receivables-to-payables gap — are compounding. Each one grows more acute as a manufacturer scales. Managing working capital proactively, and knowing where to access additional capital when needed, isn't just good financial practice. For manufacturers who can't wait on a traditional bank's timeline or credit box, working with a capital advisor like Stirling Capital Group can open access to asset-based lending, inventory financing, and other structures built specifically for operational gaps.

Frequently Asked Questions

Why do manufacturing companies need working capital?

Manufacturers need working capital to cover the gap between when they pay for inputs — materials, labor, overhead — and when they collect from customers. That gap exists in every production cycle and grows larger as order volume increases.

What are the main sources of working capital for manufacturing companies?

Primary sources include retained earnings, revolving lines of credit, invoice factoring, asset-based lending (against receivables or inventory), and purchase order financing. Manufacturers that don't qualify for traditional bank products often turn to private or non-bank lenders instead.

What factors influence working capital needs in manufacturing?

The main drivers are production cycle length, inventory turnover rate, customer payment terms (DSO), supplier payment terms (DPO), seasonality, growth rate, and how capital-intensive the process is.

What is a healthy working capital ratio for a manufacturer?

A current ratio between 1.5 and 2.0 is considered sound. CSIMarket data puts the miscellaneous manufacturing sector at approximately 1.7x — high enough to meet short-term obligations without leaving excess cash sitting idle.

What happens when a manufacturer runs out of working capital?

Payroll and supplier invoices go unpaid, production lines slow or stop, and customer orders get missed. Businesses in this position often resort to expensive emergency credit — at rates that erode margins further — while customer relationships take lasting damage.