Most founders treat these as interchangeable. They're not. The type of investor you bring on shapes your ownership structure, the growth pace you're expected to maintain, and whether your incentives actually align with theirs. Choosing the wrong one can create friction from the very first board meeting.

This article breaks down exactly how VC and growth equity differ — and gives you a practical framework to determine which one fits where your business actually is right now.

Key Takeaways

- Company stage is the decisive factor: VC targets unproven models; growth equity targets businesses that have already found product-market fit

- VC funds are built to absorb a high failure rate — growth equity investors expect the majority of bets to pay off

- Both strategies typically take minority equity stakes, leaving founders with meaningful ownership and operational control

- VC chases outsized multiples (top funds average nearly 70x on winners); growth equity targets steadier 3–5x returns

- Return profile signals risk tolerance: VC suits moonshots, growth equity suits proven businesses scaling predictably

- The right fit depends on your revenue, unit economics, and how much dilution and risk pressure you're willing to accept

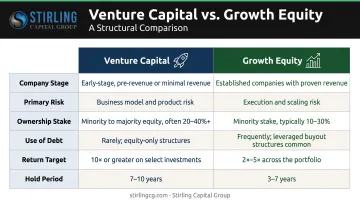

Growth Equity vs. Venture Capital: Quick Comparison

Here's a side-by-side view of how these two strategies differ across the dimensions that matter most to founders.

| Dimension | Venture Capital | Growth Equity |

|---|---|---|

| Company Stage | Pre-revenue or early-revenue; still finding product-market fit | Proven model, established traction, positive unit economics |

| Primary Risk | Market risk + product risk (will this work at all?) | Execution risk (can the team scale what's working?) |

| Ownership Stake | Minority stake; dilution compounds across multiple rounds | Minority stake; founders typically retain operational control |

| Use of Debt | Almost entirely equity-based | Primarily equity; some mature companies add modest debt |

| Return Target | High multiples on select winners; accepts high failure rate | ~3–5x returns; expects most portfolio companies to perform |

| Hold Period | 10+ years, given early entry | ~5 years |

Ultimately, the two strategies diverge on one question: what stage of risk is the investor being asked to take on? Deal structure follows from that answer.

What Is Venture Capital?

Venture capital is an equity investment strategy targeting early-stage companies — often pre-revenue or pre-profitability — in exchange for a minority ownership stake. VC is most relevant when founders are still validating their idea, assembling their team, and searching for product-market fit. Investors typically receive preferred equity with special protective provisions.

The VC Risk Model

VC funds are built around a mathematical reality: most investments will fail or return minimal capital. According to Harvard Business School, approximately 75% of VC-backed firms do not return investors' capital, with 30–40% liquidating entirely.

The economics only work because of power law outcomes. Andreessen Horowitz research using Horsley Bridge data found that roughly 6% of investments — representing just 4.5% of dollars deployed — generated approximately 60% of total returns. In great funds, home-run investments averaged nearly 70x returns.

This shapes everything about how VCs operate:

- Large, diversified portfolios to increase the odds of catching a breakout

- Pressure toward hyper-growth over profitability (they need outsized exits to make the math work)

- Tolerance for high loss rates across the portfolio

The Two Risks VCs Accept

VCs take on two types of risk that most other investors won't touch:

- Market risk — Will enough people actually want this product?

- Product risk — Can the team build what they're promising?

CB Insights' post-mortem analysis of failed startups found "no market need" consistently among the top failure reasons — direct evidence that these risks aren't theoretical.

When VC Makes Sense

VC is the right fit when your company is:

- Pre-revenue or very early in the revenue journey

- Operating in a large, potentially disruptive market

- Primarily using capital for product development, team building, and initial market entry

- Comfortable with aggressive dilution across multiple rounds and constant re-fundraising pressure

Sectors where VC concentration is highest:

- Early-stage AI and software startups

- Biotech companies in pre-clinical stages

- Fintech companies building new financial infrastructure

- Consumer tech platforms

What these sectors share is the expectation of massive scale. That expectation comes with real consequences for founders: successive rounds dilute ownership substantially, and the fund's need for high-multiple returns often pushes toward aggressive expansion before unit economics are proven.

What Is Growth Equity?

Growth equity targets companies that have already cleared the hardest hurdles: meaningful revenue, positive unit economics, and a proven business model. The capital isn't for figuring out what works — it's for scaling what's already working into new markets, larger sales organizations, or additional product lines.

As Cambridge Associates characterizes it, growth equity sits between VC and traditional private equity buyouts — it takes minority stakes, uses little to no leverage, and targets companies with demonstrated growth rather than turnaround potential. Cambridge Associates defines growth equity companies as typically generating annual revenue growth in excess of 10%, often exceeding 20%.

The Growth Equity Risk Model

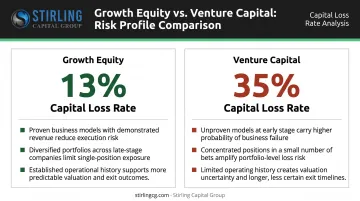

Unlike VC, growth equity investors expect most of their portfolio companies to succeed. Cambridge Associates' analysis found a capital loss ratio of just 13% for growth equity versus 35% for venture capital — a meaningful difference that reflects the lower inherent risk of backing businesses with proven models.

This lower loss rate allows growth equity funds to run more concentrated portfolios, which in turn means investors can be more hands-on — actively providing value in hiring, financial planning, go-to-market strategy, and operational scaling.

A 2025 Georgetown University Baratta Center study reported that growth equity showed the best median Net IRR and MOIC among private equity strategies studied, though the researchers noted the performance gap lacked strong statistical significance across all strategies.

Return Expectations and Secondary Liquidity

Growth equity investors frequently purchase a mix of new (primary) shares and existing (secondary) shares — which means founders can take some liquidity off the table without a full exit. That option is rarely available in early VC rounds.

Growth equity managers typically target gross returns of 3–5x on invested capital, with liquidity events typically initiated after 3–5 years — a shorter and more predictable horizon than VC.

When Growth Equity Makes Sense

Growth equity fits when your business has:

- Clear product-market fit with a repeatable go-to-market engine

- Recurring revenue or predictable customer acquisition economics

- A path to profitability (if not already there)

- Capital efficiency — the business isn't burning cash without line of sight to returns

Common sectors include:

- Fintech companies scaling into new geographies

- Healthcare businesses with approved products expanding distribution

- SaaS companies building out enterprise sales teams

- E-commerce operators optimizing logistics and supply chain

Growth equity is typically a company's final private raise before an IPO or strategic acquisition — pre-exit capital with a defined timeline, not the start of another fundraising cycle.

Which Is the Right Fit for Your Business?

The single most useful diagnostic is this: what is the central question your business still needs to answer?

- If the question is still "will this work?" — you're in VC territory.

- If the question is "can we scale what's already working?" — you're likely in growth equity territory.

Four Questions to Test Your Readiness

Before approaching either type of investor, work through these:

- Do we have product-market fit? Consistent retention, referrals, or organic demand — not just early enthusiasm

- Are our unit economics positive? Customer acquisition cost versus lifetime value should be moving in your favor

- Are we generating meaningful, recurring revenue? Not one-time contracts or pilot programs

- Can we reach profitability without another large raise? Or does growth require perpetual capital infusion?

If you answered yes to most of those, growth equity deserves serious consideration. If you're still working through them, VC's higher risk tolerance is probably the right match.

The Blurring Middle Ground

The boundary between late-stage VC and early growth equity has blurred significantly. According to the Q1 2026 PitchBook-NVCA Venture Monitor, Series C median deal sizes expanded to $75M, with averages reaching $124.6M — deal sizes that increasingly overlap with early growth equity territory.

Mega-funds now operate across multiple stages, so a fund's label matters less than its philosophy. Ask any prospective investor directly:

- What is your expected loss rate across your portfolio?

- How concentrated is your portfolio — and how much time do you spend per company?

- How do you support companies that don't hit aggressive growth targets?

The answers will tell you more than the fund's marketing materials.

Operating Philosophy Fit

Beyond the financial metrics, consider the working relationship you want:

VC is better aligned with founders who:

- Are targeting moonshot outcomes in massive markets

- Are comfortable with aggressive dilution across multiple rounds

- Understand that the fund's return math requires high-risk bets across the portfolio

Growth equity is better aligned with founders who:

- Prioritize capital efficiency and sustainable scaling

- Want to retain meaningful ownership through to exit

- Are looking for an investor who treats them as a long-term partner rather than one of many high-risk bets in a diversified portfolio

For many growth-stage businesses, the choice isn't binary. Combining equity with debt capital can reduce dilution while preserving runway — and the right structure depends on where the business actually stands, not on a fund's preferred deal profile. Stirling Capital Group works with growth-oriented businesses to identify that mix, drawing on a network of over 60 private lending sources alongside equity capital partners to match capital structure to business reality.

Frequently Asked Questions

What is the difference between growth equity and venture capital?

The primary difference is company stage. VC invests in early-stage, unproven businesses where market and product risk dominate. Growth equity invests in companies with proven models and positive unit economics, taking on execution risk instead. Both typically hold minority stakes and avoid heavy leverage.

What stage of company qualifies for growth equity vs. venture capital?

VC targets pre-revenue or early-revenue startups still validating product-market fit. Growth equity targets companies generating meaningful recurring revenue with proven unit economics and a clear path to profitability or scale — typically at Series C or later stages.

Do growth equity investors take control of your company?

Growth equity investors typically take minority stakes and do not acquire a controlling position. Founders and management generally retain day-to-day operational control, though the investor usually holds a board seat and standard protective provisions.

Can a company receive both VC and growth equity at different stages?

Yes, and it's common. A company typically receives VC funding in its early stages, then transitions to growth equity as it matures and demonstrates a scalable model.

What returns do growth equity investors typically target?

Growth equity investors target approximately 3–5x gross returns on invested capital over a roughly 5-year holding period. VC investors target far higher multiples (top-performing funds have averaged nearly 70x) to offset the high expected failure rate across their portfolios.

How is growth equity different from a private equity buyout?

PE buyouts acquire controlling or majority stakes using significant debt to restructure mature or underperforming companies. Growth equity takes a minority stake in high-growth companies with little to no debt, partnering with existing management rather than replacing or overriding them.

Each structure is purpose-built for a different stage of company development and a different risk profile. Before approaching any investor, understand your own stage, unit economics, and goals for ownership and control — those factors determine which path fits.

If you're unsure how equity fits into your broader capital structure — or whether debt, equity, or a hybrid makes the most sense — a conversation with a capital advisory firm is a practical first step. Stirling Capital Group offers free consultations and can be reached at 614-470-4716 or info@stirlingcg.com.